.avif)

.svg)

.svg)

The layer of payer intermediaries that quietly changes the payment methodology on your claim - and what to do about it.

You signed a contract with one entity. The remittance arrives showing payment from a different entity, at a rate that does not match what you negotiated, with a one-line explanation referencing a "repricing methodology" you have never heard of. This is the structural underpayment problem hiding in plain sight across US commercial healthcare: a layer of third-party administrators, sub-administrators, rental networks, and algorithmic repricers that sit between you and the payer named on the patient's insurance card. Each one can apply a completely different payment methodology to the same claim - and you typically do not find out until the money lands.

The scale of the problem is now visible in court records. Plaintiff providers allege that MultiPlan (rebranded as Claritev in February 2025) and its insurer partners coordinate $19 billion to $23 billion in annual underpayments through algorithmic repricing tools. A parallel federal case against Zelis is proceeding through the District of Massachusetts. The US Department of Justice filed a Statement of Interest supporting providers in March 2025. The legal landscape is shifting fast, but the operational problem the litigation describes has existed for decades.

Key takeaways

- Four categories of intermediaries can alter your payment methodology: TPAs (claims processors for self-funded plans), sub-administrators (carved-out specialty payers), rental networks/silent PPOs (your discounts leased to non-contracted payers), and repricers (algorithmic out-of-network pricing).

- Repricers now dominate out-of-network commercial claims. MultiPlan/Claritev processes more than 80% of US out-of-network claims. Zelis serves more than 750 payers and TPAs.

- Typical repricer discounts reach 61-81% off billed charges, with some claims paid as low as 1% of charges according to consolidated antitrust complaints.

- Detection requires looking in three places: the remittance itself, your contract language, and your payment data for patterns variance reports miss.

- The recovery path is multilayered. Single-claim disputes, contract enforcement, state silent-PPO regulators (14 states have specific statutes), and antitrust class action participation are all on the table.

- Algorithmic adjudication beats manual checks. A contract-based variance engine catches the silent underpayments - the ones with no remark code and no explanation - that staff reviewers will never find.

What is on this page

- The structural problem: why methodology matters more than rate

- The four categories of payer intermediaries

- The repricer problem: MultiPlan, Zelis, and the antitrust wave

- How to spot a repriced claim

- The recovery path

- Protecting against it going forward

- How MD Clarity helps

- FAQ

The structural problem: why methodology matters more than rate

Most provider contract conversations focus on the rate: what percentage of Medicare, what fee schedule, what case rate. The rate matters, but the methodology matters more. The methodology is the entire chain of logic the payer's adjudication system applies between the claim arriving and the payment going out. Modifiers, locality adjustments, bundling rules, fee schedule version, sequestration, lesser-of clauses, carve-out logic - all of these live inside the methodology.

When a claim signed under your contract gets routed through an intermediary, the methodology can change at any point in the chain. The intermediary may apply:

- A different fee schedule than the one you negotiated (often a prior year's rates, or a separately maintained schedule)

- A different bundling logic that suppresses line items you expect to pay separately

- A reference-based pricing algorithm that determines payment as a percentage of Medicare rather than your contracted rate

- A network discount that you never agreed to grant to the entity actually paying the claim

The payment that lands in your bank is the output of whichever methodology was actually applied - not the one your contract describes. Standard practice management system variance reports cannot detect this. The PM system compares the payment to a single fee schedule it knows about. It does not know that a different schedule was applied because of an intermediary in the chain. Underpayments routed through intermediaries are therefore systematically invisible in the reports most revenue cycle teams use.

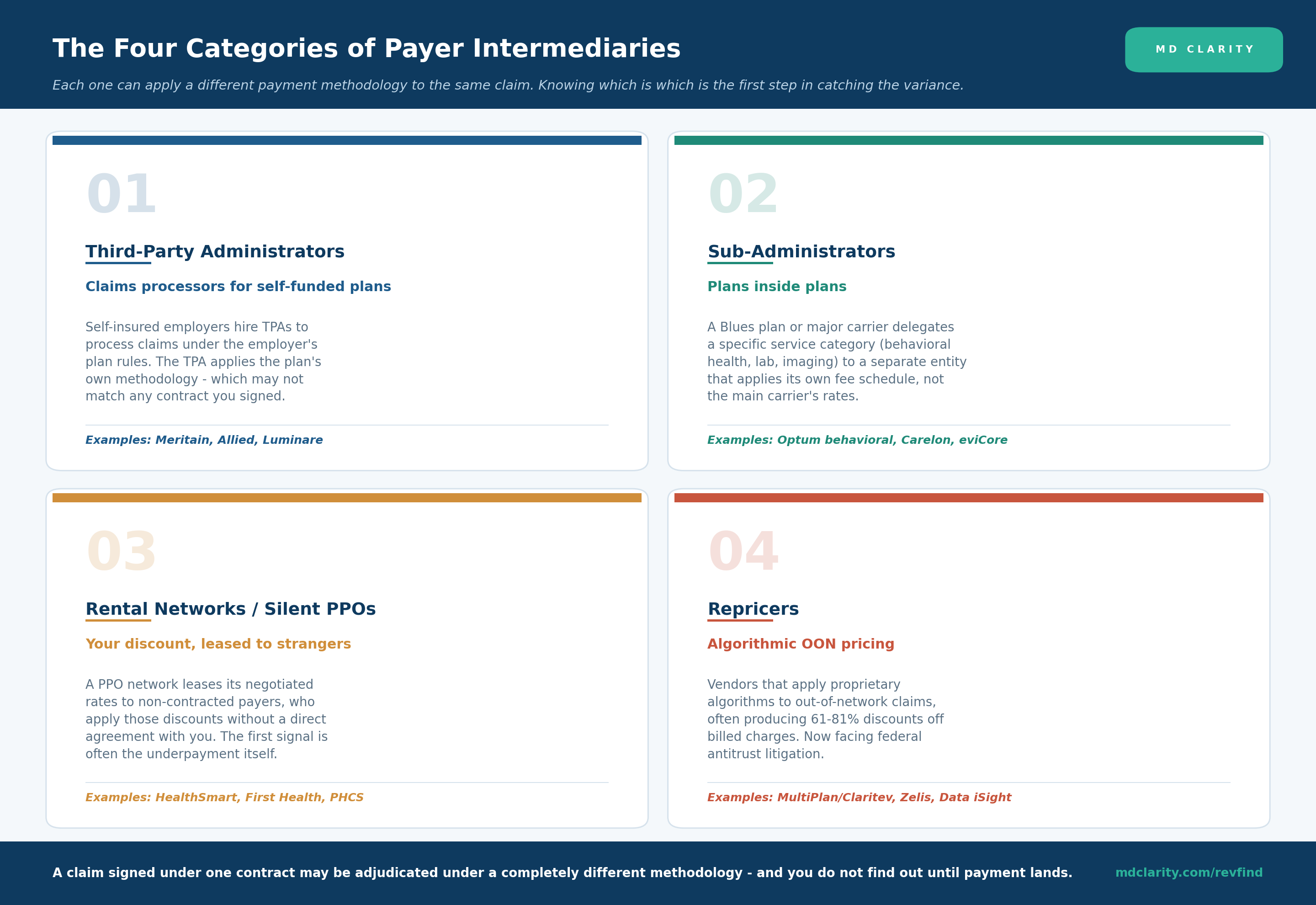

The four categories of payer intermediaries

The intermediary universe has four primary categories. The categories overlap - MultiPlan and Zelis, for example, operate in two or three of them at once - but each category creates a distinct underpayment risk that requires a distinct detection and recovery approach.

Third-party administrators (TPAs)

A TPA processes claims for a self-insured employer plan. The employer, not an insurer, is the legal payer; the TPA is the operational engine. The TPA applies the rules in the employer's plan document, which may or may not match the network contract terms a provider signed.

A Georgetown Center on Health Insurance Reforms analysis describes the structural problem well: the administrative service agreement between the TPA and the employer "generally does not provide the plan sponsor with the terms of the reimbursement agreement between the TPA and its network providers, nor a clear payment methodology for non-network claims, nor a detailed delineation of the TPA's administrative practices, including the use of third parties to reprice claims." In other words, the employer paying the bill often does not know how the TPA is calculating the payment - and the provider receiving the payment definitely does not know.

The largest commercial carriers (Aetna, Cigna, UnitedHealthcare, Anthem/Elevance) operate massive TPA arms in addition to their fully-insured business. When the carrier's TPA arm processes a self-funded employer's claim, the carrier's name appears on the card and the EOB, but the contractual relationship and methodology can be different from the carrier's standard commercial plan. This is one of the most common sources of provider confusion about why a "Cigna" claim paid differently than expected.

Sub-administrators

A sub-administrator is a layer beneath a primary payer that handles a specific service category. A typical example: a Blue Cross plan that delegates behavioral health services to a separate entity, lab services to another, and imaging to a third. Each sub-administrator applies its own fee schedule and methodology to the carved-out service line.

Common examples include Optum (behavioral health for many UHC plans), Carelon (formerly Beacon, behavioral health for Anthem plans), and eviCore (radiology and specialty management across multiple carriers).

The underpayment risk: providers contract with the primary payer and assume the primary payer's rates apply across all services. The remittance for a carved-out service comes back at the sub-administrator's rate, not the primary payer's rate. Without a separate contract review or a variance engine that knows which services are carved out to whom, the discrepancy passes through unexamined.

Rental networks and silent PPOs

A rental network is a PPO network that has contracts with providers and then leases access to those contracted rates to non-contracted payers. The non-contracted payer pays the network for access to the discount, applies the discount to your claim, and pays you the discounted amount - despite never having signed a contract with you.

The mechanism dates back to the early 1990s and has been called variously "silent PPOs," "ghost PPOs," "blind PPOs," and "rental networks." The Texas Medical Association and other state medical associations have published warnings about silent PPOs for more than 15 years. As of 2026, 14 states have laws attempting to limit or prohibit the practice. The states include Connecticut, Colorado, Florida, Indiana, Ohio, Arkansas, California, Kentucky, Louisiana, Maryland, Minnesota, North Carolina, Oklahoma, South Carolina, Texas, and Virginia.

State laws help but do not solve the problem. Most provider contracts contain "all-payer" or "affiliate" language allowing the PPO to lease the network to entities not specifically named in the contract. Courts and regulators must then assess whether the provider intended to allow the leasing arrangement when signing broadly worded contract language.

The first signal of a silent PPO is almost always the underpayment itself. A patient presents with an unfamiliar insurance card, the claim is submitted, and the remittance returns at the discounted rate of a contract the patient's payer should not have access to.

Repricers

A repricer does not hold provider contracts. It is a pure pricing service. Insurers and TPAs route claims (typically out-of-network claims, though increasingly some in-network) through the repricer's platform. The repricer applies a proprietary algorithm, often a reference-based pricing methodology calibrated against Medicare rates or another benchmark, and returns a "repriced" amount that the payer then uses as the basis for payment.

The dominant repricers in the US market:

- MultiPlan / Claritev - the largest player. Processes more than 80% of US commercial out-of-network claims by volume according to consolidated complaints. Rebranded as Claritev in February 2025 after roughly 45 years operating as MultiPlan.

- Zelis - serves more than 750 health plans, TPAs, and self-funded employers. Acquired Payer Compass and its Visium reference-based pricing platform in 2022.

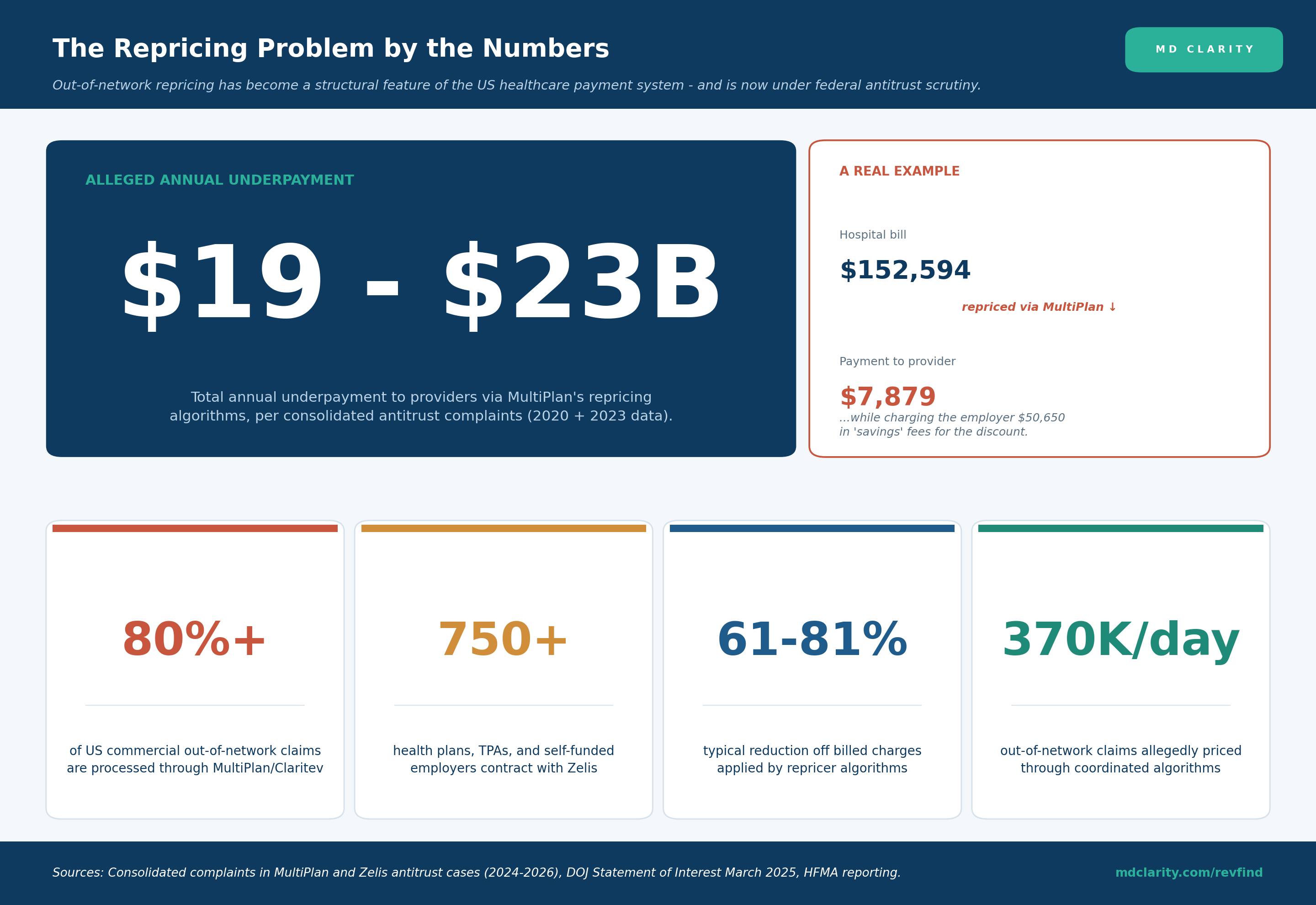

- Data iSight - a MultiPlan-owned tool that the company markets as producing 61-81% discounts off billed charges while maintaining 89-98% provider acceptance rates.

- Viant - another MultiPlan-owned platform applying similar methodology.

- Payer Compass - now part of Zelis, focused on reference-based pricing for self-funded plans.

The repricer model is now the most active area of federal antitrust litigation in healthcare, and it deserves its own section.

The repricer problem: MultiPlan, Zelis, and the antitrust wave

Out-of-network repricing has moved from a niche operational concern to a federal antitrust priority over the last 24 months.

The MultiPlan antitrust litigation - consolidated in the Northern District of Illinois - alleges that MultiPlan (now Claritev) acted as the "hub" in a hub-and-spoke price-fixing arrangement, coordinating out-of-network reimbursement rates among major commercial insurers that would otherwise compete on price. Plaintiff providers in the consolidated complaint allege $19 billion in annual underpayments in 2020 alone, with a later complaint alleging $22.9 billion in 2023 and $6.4 billion in a single quarter of 2024. The complaints describe more than 370,000 out-of-network claims daily processed through coordinated algorithmic pricing.

A federal judge declined to dismiss the MultiPlan case in June 2025, specifically noting that algorithm-driven pricing coordination can meet the legal threshold for anticompetitive conduct even without explicit communication between competitors. The Department of Justice filed a Statement of Interest supporting the providers' position in March 2025.

The Zelis litigation runs in parallel. In a Massachusetts case filed in March 2025, provider plaintiffs allege the same hub-and-spoke pattern through Zelis's repricing platform. A federal judge declined to dismiss the case in March 2026, allowing it to proceed to discovery. Court filings describe Zelis repricing a claim at 88% below billed charges and other claims paid at 1% of charges.

The most-cited illustrative example from the litigation: UnitedHealthcare used MultiPlan to reduce a $152,594 hospital bill to $7,879 - a 95% reduction - then charged the self-funded employer that owed the bill $50,650 as a "savings" fee for the discount. The provider received $7,879. The employer paid $50,650 for the privilege of paying $7,879 less. MultiPlan kept the $50,650.

This pattern - the repricer charging the employer a fee proportional to the discount the provider absorbs - is at the heart of the antitrust theory. As HFMA's coverage of the litigation notes, "the entire third-party repricing industry may need to restructure" if courts ultimately find the model constitutes price fixing. Damages in the consolidated MultiPlan case are subject to mandatory tripling under federal antitrust law.

For provider revenue cycle teams, the litigation is not just an interesting news story. It validates a longstanding suspicion - that the unexplained low payments labeled "repriced per methodology" had a coordinated origin - and it opens recovery paths that did not exist before.

How to spot a repriced claim

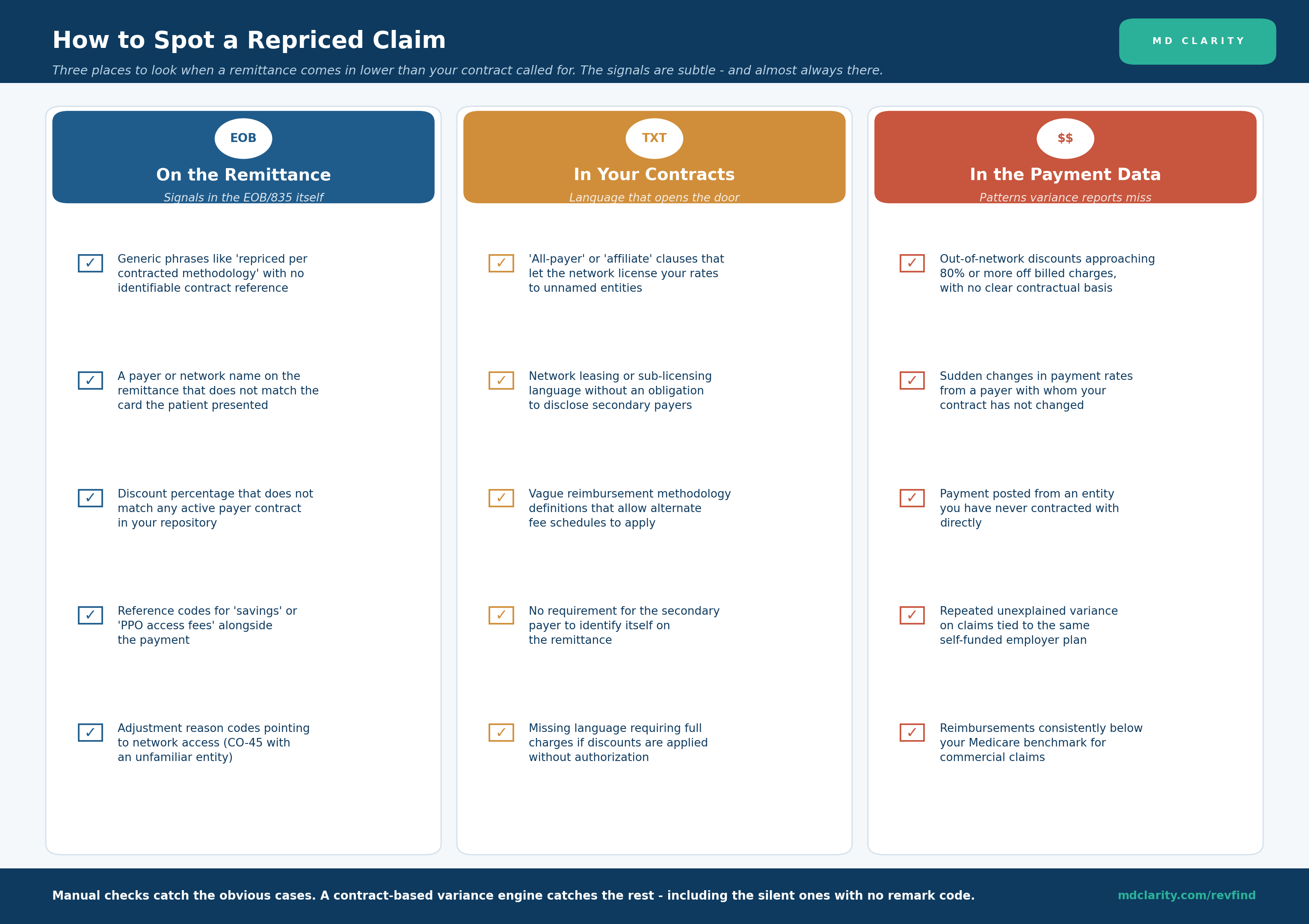

The detection problem with repriced claims is that they often look like normal paid claims. The remittance arrives, the claim closes in the patient accounting system, and the gap between contracted and actual payment hides in the difference. Three categories of signals help surface what would otherwise stay invisible.

On the remittance itself. The first place to look is the EOB or 835 transaction. Generic language like "repriced per contracted methodology" with no identifiable contract is a red flag. So is a payer or network name on the remittance that does not match the card the patient presented - often a sign that a TPA or sub-administrator handled the claim. A discount percentage that does not match any contract in your repository is another tell. Reference codes for "savings achieved" or "PPO access fees" alongside the payment indicate a repricer was involved.

In your contracts. Many underpayments via rental networks and repricers are technically permitted by contract language the provider signed years ago. "All-payer" or "affiliate" clauses let the network license rates to unnamed entities. Network leasing or sub-licensing language without an obligation to disclose secondary payers leaves a door wide open. Vague reimbursement methodology definitions allow alternate fee schedules to apply. The absence of language requiring full charges if discounts are applied without authorization removes your main lever for disputing the application of a rented discount.

In the payment data. Some patterns only become visible in aggregate. Out-of-network discounts approaching 80% or more off billed charges with no clear contractual basis warrant investigation. Sudden changes in payment rates from a payer with whom your contract has not changed often indicate a switch in repricing methodology. Payments posted from an entity you have never directly contracted with point to a TPA or sub-administrator arrangement. Repeated unexplained variance on claims tied to the same self-funded employer plan suggests a TPA applying a different methodology than the network rate. Reimbursements consistently below your Medicare benchmark for commercial claims point toward reference-based pricing being applied via a repricer.

The honest answer about manual detection: it catches the obvious cases and misses the rest. The silent ones - claims paid at a different rate with no remark code, no denial signal, and a generic explanation - are systematically invisible to anyone reviewing remittances by hand. A contract-based variance engine that replicates payer adjudication at the charge line is the only mechanism that catches them reliably.

The recovery path

Once a repriced or alternate-methodology claim is identified, four recovery paths exist. Most mature underpayment programs work them in parallel.

1. Single-claim dispute. File a formal underpayment dispute citing the specific contract that should have applied, the rate that should have been paid, and the variance. Attach the contract clause and fee schedule exhibit. Demand payment per the contracted methodology. Many TPA and sub-administrator underpayments resolve at this stage if the provider has the contract data to make a precise case.

2. Contract enforcement. If the variance pattern persists across multiple claims from the same payer or TPA, the issue is structural rather than per-claim. Escalate through provider relations channels, then through legal counsel. The Aetna/Optum "dummy codes" case (settled after the Fourth Circuit reinstated provider claims that Aetna had disguised subcontractor fees as medical claims) demonstrates that breach-of-fiduciary-duty theories can apply to TPA arrangements affecting self-funded plans.

3. State silent-PPO complaints. In the 14 states with anti-silent-PPO statutes, providers can file regulatory complaints when discounts are applied without authorization or transparency. State laws often require disclosure of which secondary payer accessed a discount and prohibit transfer of pricing information without provider consent.

4. Antitrust class action participation. Both the MultiPlan/Claritev and Zelis antitrust cases are class actions in active discovery. Providers should evaluate exposure to the defendants' claims, preserve relevant claims data, and consider direct-action or class participation given the potential for treble damages under federal antitrust law. The ArentFox Schiff healthcare antitrust roundup provides current guidance on preservation and participation strategy.

In every path, the foundation is the same: precise documentation of the gap between contracted rate and actual payment, anchored in the specific contract clause that should have applied. Without that documentation, every path collapses into generic complaint. With it, the appeals process tilts in the provider's favor and the antitrust class evidence base grows.

Protecting against it going forward

Detection and recovery address claims that have already been underpaid. Prevention addresses the next contract cycle and the operational discipline that catches problems sooner.

Contract language. At renewal, push back on all-payer and affiliate clauses that let networks lease your rates to unnamed entities. Require the network to identify on each remittance which secondary payer accessed your discount. Require advance notice of any network-rental arrangement. Include language that obligates payers to pay full charges if discounts are applied without explicit authorization. These provisions exist in well-drafted contracts but rarely appear in the standard agreement a payer offers; they need to be negotiated in.

Monitoring infrastructure. Build or buy the variance detection layer that operates at the charge line. Variance reports from the practice management system are not enough. The detection has to replicate payer adjudication logic across every contract and surface the gap on every claim, not just sampled audits. This is exactly the workload that purpose-built contract management and revenue optimization software handles.

Continuous payer scorecards. Track payment integrity by payer over time. A payer whose denial rate is unchanged but whose paid rate is dropping is being routed through a different methodology somewhere in the chain. Quarterly variance trending by payer surfaces these shifts before they compound across thousands of claims.

Contract repository discipline. Most variance disputes lose at the documentation stage. Maintain a digital repository of every executed payer contract, fee schedule version, and amendment, with the ability to search and produce the exact clause that supports any given dispute within minutes. The repository is the foundation for both prevention and recovery.

How MD Clarity helps

The structural underpayment problem described in this article - claims signed under one methodology being adjudicated under another - is exactly what RevFind was built to detect.

RevFind digitizes the full contract portfolio (payer agreements, fee schedules, carve-outs, and lesser-of clauses) and runs every remittance through a pricing engine that replicates payer adjudication at the charge-line level. When the actual paid amount diverges from what the applicable contract called for, RevFind flags the variance - whether the cause is a TPA applying the wrong methodology, a sub-administrator using its own fee schedule, a rental network lending out a discount, or a repricer running an algorithm. The audit trail traces every calculation back to the specific contract clause that should have produced the expected amount.

For revenue cycle teams without the headcount to pursue every flagged variance, Underpayment Recovery Services supplies the specialist layer. Payer reimbursement experts review each flagged claim, build the contract-anchored appeal, and pursue recovery through escalation - including direct negotiation with the responsible TPA or payer and coordination with legal counsel when antitrust or breach-of-contract claims are in play. The combination converts the structural problem from invisible revenue leakage into a tracked, recoverable cash stream.

Get a demo to see RevFind detect a repricer-driven variance in real time and trace it back to the contract clause that should have applied.

FAQs

What is a third-party repricer in healthcare?

A third-party repricer is a vendor that applies a proprietary algorithm or fee schedule to determine what an insurer or self-funded plan will pay on a claim, typically for out-of-network services. Repricers do not have direct contracts with providers. They sit between the payer and the remittance, applying discounts that often reach 61-81% off billed charges. MultiPlan (now Claritev) and Zelis are the two dominant repricers in the US market

What is the difference between a TPA, a sub-administrator, and a repricer?

A TPA (third-party administrator) processes claims for self-funded employer plans using the employer's money and plan rules. A sub-administrator handles a specific service category - behavioral health, lab, imaging - delegated by a major carrier and applies its own fee schedule. A repricer is a pure pricing service that applies algorithmic discounts to out-of-network claims without holding provider contracts. The categories can overlap - MultiPlan and Zelis, for example, operate across multiple categories.

How do you know if a claim was repriced through a third party?

Look for three signals. On the remittance: generic phrases like "repriced per contracted methodology," payer names that do not match the patient's insurance card, and discounts that do not match any contract you signed. In your contracts: "all-payer" or "affiliate" clauses that allow network leasing. In your payment data: out-of-network discounts approaching 80% or more with no contractual basis, or sudden rate changes from a payer whose contract has not changed.

Can providers recover underpayments caused by repricers?

Yes, through several paths. First, dispute the specific claim by citing the contract that should have applied and demanding payment per its terms. Second, escalate through provider relations and, if necessary, legal counsel. Third, in the 14 states with anti-silent-PPO statutes, file a regulatory complaint. Fourth, evaluate participation in active class action litigation against MultiPlan/Claritev and Zelis, which allows for treble damages under federal antitrust law. The key in every path is precise variance documentation showing the gap between contracted rate and actual payment.

What is a silent PPO and how is it different from a regular PPO?

A regular PPO has direct contracts with both providers (who agree to discounts in exchange for in-network volume) and payers (who pay the PPO to access those discounts). A silent PPO is the same structure with one crucial difference: the PPO leases provider discounts to additional payers who have no direct contract with the provider. The provider gave the discount expecting in-network referrals from the contracting payer, but a non-contracting payer is also applying the discount. The "silent" label refers to the lack of disclosure to the provider.

What contract language helps prevent rental network and silent PPO underpayments?

Negotiate against "all-payer" clauses that let a network license your rates to unnamed entities. Require the network to identify on each remittance which secondary payer accessed your discount. Require advance notice of any network-rental arrangement. Include language obligating payers to pay full charges if discounts are applied without explicit authorization. These provisions rarely appear in the standard agreement a payer offers - they need to be negotiated in.

Get paid in full by bringing clarity to your revenue cycle

Related Posts

Subscribe to the

Healthcare Clarified newsletter

Get the latest insights on RCM and healthcare policy in your inbox