.avif)

.svg)

.svg)

A payer contract audit after a physician practice acquisition is a structured review of every payer agreement at the acquired entity to confirm contracted rates, identify variances against actual payments, surface compliance risks, and prepare for harmonization with the MSO's master agreements. Done in the first 90 days, the audit typically recovers 1 to 3 percent of net patient revenue in underpayments and surfaces three to five contracts that warrant renegotiation or termination.

This is a tactical guide for MSO VPs of managed care, directors of revenue cycle, and the consultants who support physician practice integrations. It walks through the 5-step audit framework, the red flags to look for, and the action plan that turns audit findings into recovered revenue and stronger payer positioning.

What is a payer contract audit after a physician practice acquisition?

A post-acquisition payer contract audit is a comprehensive review of three things: the contract terms themselves (assignability, termination, escalators, renewal), the fee schedules attached to each contract (rates by CPT, modifier, place of service), and the payment performance of each payer against those contracted rates over the trailing 12 to 24 months.

It is distinct from a billing or coding audit (which examines whether the practice billed correctly) and from a payer-initiated audit (where the payer reviews the practice's claims). A contract audit asks the inverse question: is the payer paying what they agreed to pay, and are the contract terms still acceptable to the MSO?

This audit is the foundation of post-acquisition revenue cycle integration. Without it, every other RCM integration activity is operating on bad data.

Why audit payer contracts after acquiring a physician practice?

Three reasons make this audit non-negotiable for MSO platforms.

First, most acquired practices have never done one. Independent practices rarely have the tooling, time, or expertise to load every contract into a system and compare actual payments against contracted rates at the CPT level. Healthcare underpayments accumulate at 1 to 3 percent of net patient revenue annually, which compounds across an MSO platform.

Second, payer contracts often don't survive acquisitions intact. Healthcare attorneys at the Association of Corporate Counsel note that in an asset purchase, the buyer can decline to accept assignment of provider agreements and instead apply as a new provider, while in a stock purchase, change of control provisions may treat the acquisition the same as an outright transfer. The legal structure of the deal determines which contracts survive, which require payer consent, and which need to be re-papered entirely.

Third, payer behavior has gotten worse. Initial claim denial rates hit 11.8 percent in 2024, and nearly 88 percent of revenue cycle leaders cite payer challenges as their top stressor. Inherited contracts that were marginal three years ago are often unworkable today.

When should a payer contract audit start?

The audit should ideally begin during pre-close diligence (Phase 1 of the post-acquisition integration framework), with full execution completed within 90 days of close.

Pre-close diligence catches the worst contracts before the deal terms are locked. Findings from a pre-close audit can support purchase price adjustments, hold-back terms, or escrow provisions tied to specific renegotiation milestones. McKinsey research shows that due diligence fails to provide an adequate roadmap for capturing synergies 42 percent of the time, and the contract audit is one of the most common gaps.

When pre-close access is not granted (often the case in competitive auction processes), the audit becomes the first work stream on Day 1 post-close and should be substantially complete by Day 90.

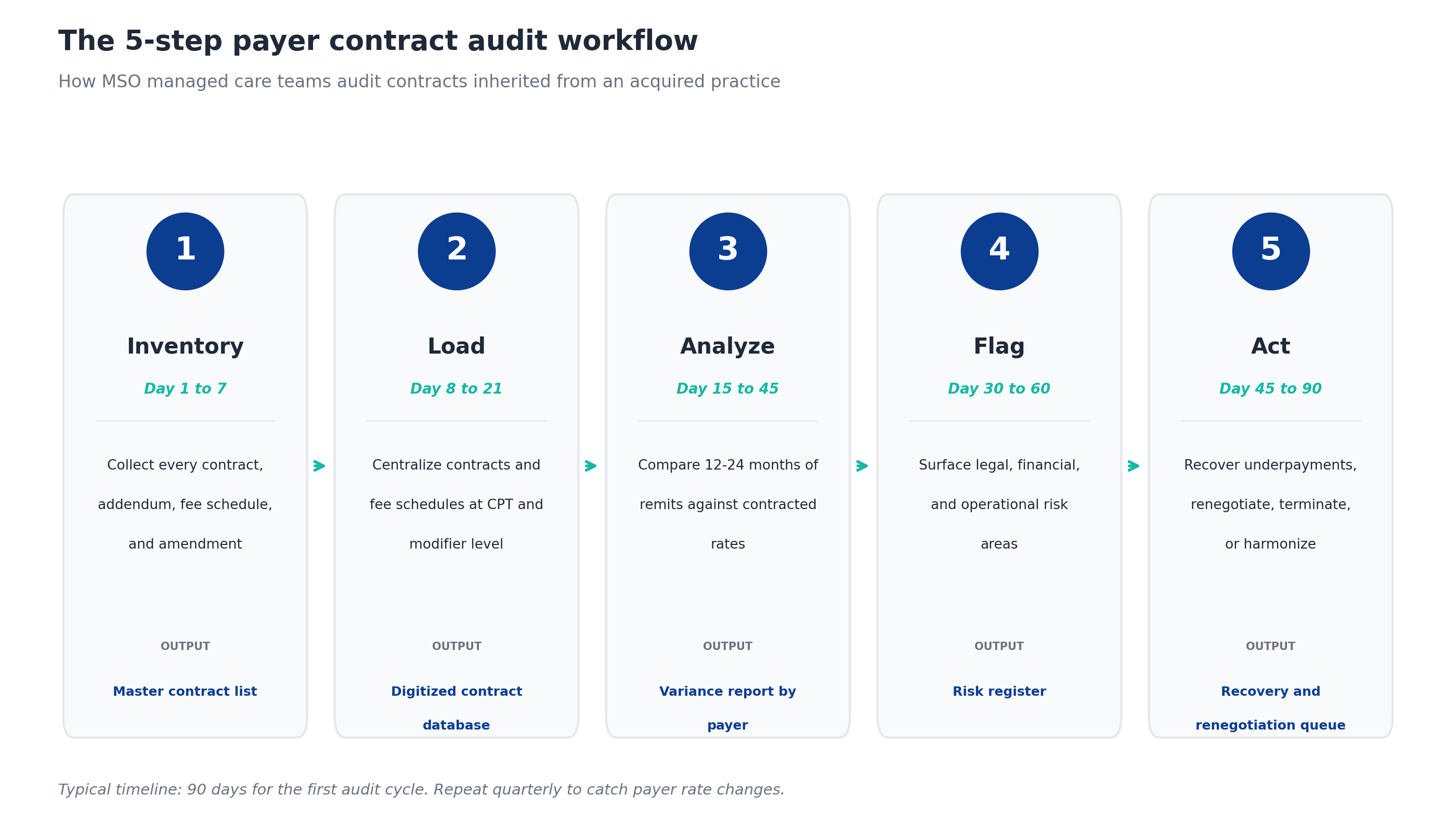

The 5-step payer contract audit framework

Disciplined audits run on a repeatable 5-step process. Each step has a clear output that becomes the input to the next.

Step 1: Inventory every contract

The first job is to find every payer agreement that governs reimbursement at the acquired entity. This is harder than it sounds. Acquired practices often store contracts in shared drives, paper file cabinets, and the personal email of a long-tenured office manager. The full inventory includes:

- Master contracts for every commercial payer, Medicare Advantage plan, Medicaid managed care plan, and direct-contracted employer

- Amendments and addendums, especially fee schedule updates from the last five years

- Single case agreements for out-of-network procedures

- Network participation agreements through IPAs, ACOs, or clinically integrated networks

- Capitation and value-based care agreements, including risk-sharing terms

Common gaps the audit team will surface:

- Contracts that exist but cannot be located

- Amendments signed but never filed

- Verbal rate increases never documented in writing

- Network participation through entities the practice forgot it joined

If a contract cannot be produced, the practice is operating on whatever rates the payer chooses to apply. That is a finding in itself.

Step 2: Load contracts and fee schedules into one system

Once contracts are inventoried, they need to be digitized into a single contract management platform with fee schedules captured at the CPT, modifier, and place of service level. Physician fee schedules are intricate, with complex modifier logic and varying rates by location and credentials, so generalist contract software often fails to capture the granular details that drive revenue.

The fields that matter:

- Effective and termination dates

- Renewal terms (auto-renewal vs. explicit renewal)

- Notice requirements for termination

- Change of control and anti-assignment provisions

- Rate methodology (percentage of Medicare, fixed dollar, case rate, capitation)

- CPT-level fee schedules with modifiers

- Carve-outs for specific services, sites, or providers

- Annual escalators and rate refresh provisions

- Timely filing and appeal deadlines

- Lesser-of clauses tied to billed charges

This is also the step where the audit team flags contracts that exist but lack a current fee schedule. That gap alone is worth fixing, because the practice cannot detect underpayments against a fee schedule it does not have.

Step 3: Compare contracted rates to actual payments

With contracts loaded, the audit team runs a variance analysis comparing every paid claim from the last 12 to 24 months against the contracted rate for that CPT, modifier, and payer. This is where the underpayments surface.

The methodology:

- Pull 12 to 24 months of remits from the practice management system

- Match each line item to the corresponding contract and fee schedule

- Calculate the variance (actual paid vs. contracted) at the line level

- Aggregate variances by payer, by CPT, by provider, and by site

- Sort by total dollar exposure

A 1 percent variance on a $50 million net patient revenue practice is $500,000 of recurring annual leakage. The aggregate often understates the per-payer picture, where some payers may be underpaying 3 to 5 percent on specific procedure families while overall variance looks acceptable.

One orthopedics MSO running this analysis across multiple practices found $10.3 million in underpayments and used the results to drive both recovery efforts and payer renegotiations.

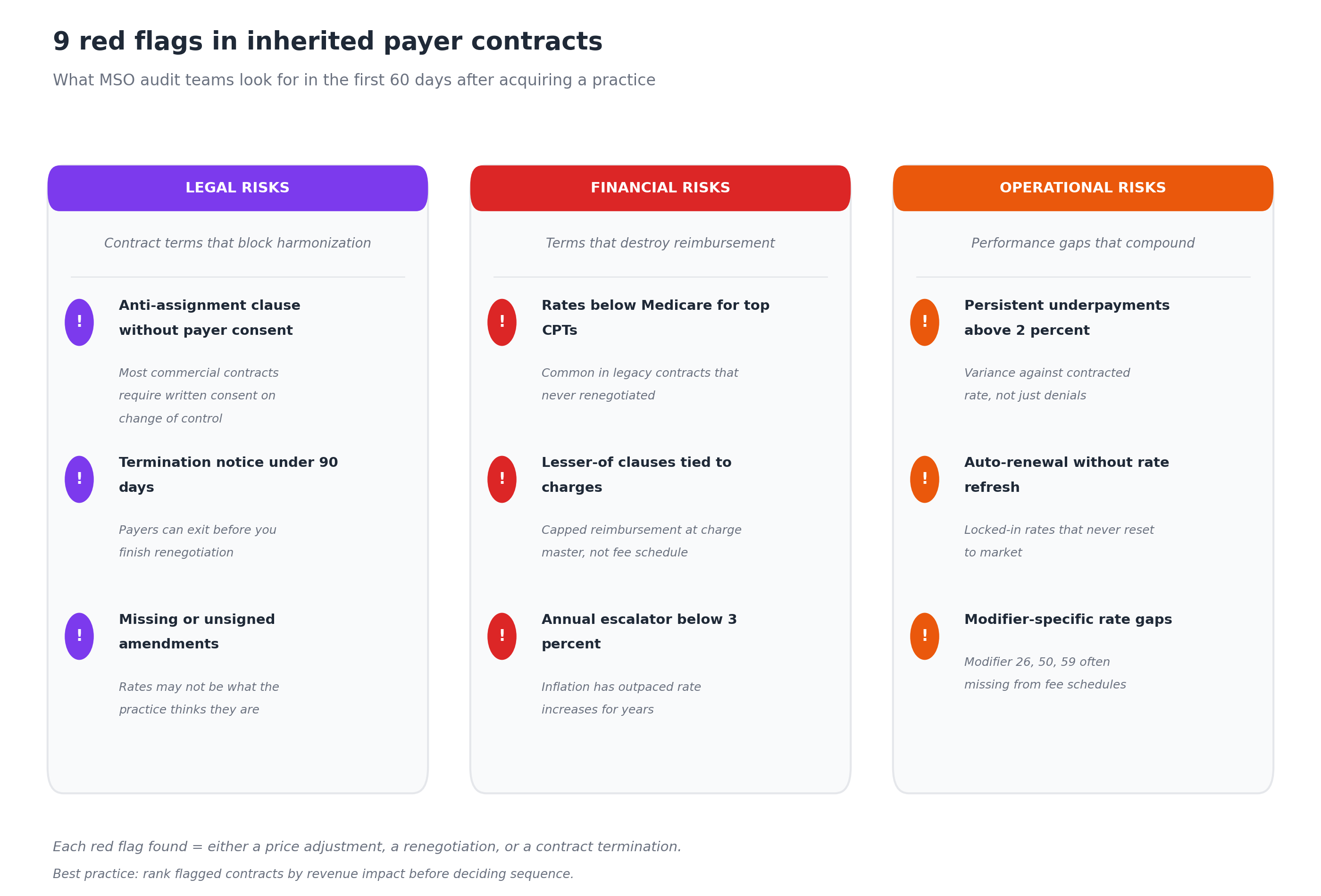

Step 4: Identify red flags and risk areas

Beyond pure dollar variance, the audit team flags contracts with terms that pose legal, financial, or operational risk. Some of these matter more than the immediate dollar impact because they constrain the MSO's ability to renegotiate, terminate, or harmonize the contract later.

Legal risks

- Anti-assignment clause without payer consent. Most commercial payer contracts contain provisions that require written consent on change of control. Baker Donelson's analysis notes that anti-assignment clauses may trigger a breach if consents are not obtained, and non-assignable contracts where consent is not obtained are sometimes excluded from the transaction altogether. If the practice's deal closed without payer consent, the contract may be voidable.

- Termination notice under 90 days. Polsinelli healthcare attorneys have noted that contract termination can be a "capital punishment outcome" for practices and can occur with little notice. Short notice windows mean a payer can exit before the MSO finishes renegotiation.

- Missing or unsigned amendments. When amendments exist in payer records but not in practice records (or vice versa), the actual contracted rates are unclear. This creates exposure on both underpayment recovery and renegotiation.

Financial risks

- Rates below Medicare for top CPTs. Common in legacy contracts that haven't been renegotiated in 5 to 10 years. These are immediate renegotiation candidates.

- Lesser-of clauses tied to charges. Some contracts pay "the lesser of contracted rate or billed charges." If the practice's charge master is below the fee schedule for any CPT, the payer pays the lower charge amount. This is a stealth leakage source that contract management platforms can detect during ingestion.

- Annual escalator below 3 percent. With healthcare inflation persistently above 3 percent, escalators that lag inflation produce real-dollar rate erosion every year.

Operational risks

- Persistent underpayments above 2 percent. Surfaced in Step 3. This is variance against contracted rate, not denial rate. Underpayments are often ignored because payments arrive (just below contract), unlike denials which generate clear alerts.

- Auto-renewal without rate refresh. Contracts that auto-renew with no built-in rate review lock in below-market rates indefinitely.

- Modifier-specific rate gaps. Modifier 26 (professional component), modifier 50 (bilateral procedure), and modifier 59 (distinct procedural service) are commonly missing from fee schedules or incorrectly priced. These gaps disproportionately hit procedural specialties.

Step 5: Build the action plan

The audit produces three deliverables, in priority order: a recovery queue, a renegotiation queue, and a termination/harmonization decision log.

Recovery queue

Every underpayment dollar identified in Step 3 should be routed to a recovery workflow. Underpayment recovery typically operates on payer-specific timely filing deadlines, often 90 to 180 days from the original payment. Older variances may be unrecoverable, which is why running the variance analysis quickly matters.

Recovery work should be assigned by payer (not by acquired entity), so the team building expertise on a particular payer's appeals process can apply that knowledge across the platform.

Renegotiation queue

Contracts flagged with financial red flags (below-Medicare rates, lesser-of clauses, weak escalators) go into a renegotiation queue ranked by revenue impact. Renegotiation effort is finite, so prioritization matters.

The renegotiation playbook benefits from MSO platform scale: higher patient volumes, broader geographic reach, and consolidated negotiating leverage from the parent organization. PE-backed MSOs use this leverage to negotiate higher reimbursement rates than independent practices typically achieve.

Termination and harmonization decisions

Some inherited contracts should not be renegotiated. They should be terminated and the providers added to the MSO's master contracts with that payer. The audit findings determine which contracts fit that path:

- Inherited contracts with rates materially below the MSO master contract

- Contracts where anti-assignment issues create ongoing legal risk

- Contracts with non-strategic payers (low volume, problematic operations)

Harmonization decisions also require coordination with credentialing, since adding the acquired providers to the MSO's master contracts requires payer-by-payer credentialing under the MSO TIN.

Common findings in inherited payer contracts

After many MSO audits, certain patterns repeat:

- Two to four payers account for most underpayments. The variance analysis rarely shows uniform leakage. Usually a small number of payers are systematically underpaying on a specific procedure family or modifier combination.

- Procedural specialties have the highest exposure. Orthopedics, ophthalmology, gastroenterology, and cardiology consistently surface larger underpayment dollars because their fee schedules are more complex and modifier-dependent.

- The "best contract" the practice was proud of often isn't. Practices that boast about strong commercial relationships sometimes have the worst contracts in absolute terms, because they renegotiated once a decade ago and never reset.

- Medicare Advantage contracts are usually the weakest. Acquired practices often signed into MA contracts at percent-of-Medicare rates without realizing how MA plan design erodes the effective rate over time.

- At least one contract is unsigned, expired, or unfindable. This is so common it should be assumed as a working hypothesis.

How long does a payer contract audit take?

A complete first-cycle audit on a single acquired practice typically takes 60 to 90 days from contract collection to action plan delivery. The phasing breaks down approximately as:

- Days 1 to 14: Inventory. Collecting all contracts and amendments takes longer than expected, especially when documents are scattered or the office manager has limited bandwidth.

- Days 8 to 28: Load. Digitizing contracts and fee schedules into a contract management system. The biggest delays are usually contracts with non-standard fee schedule formats (PDF tables, embedded spreadsheets, percent-of-Medicare with complex carve-outs).

- Days 15 to 45: Analyze. Variance analysis runs faster once data is loaded, but the initial reconciliation against the practice's remit history can surface data quality issues that take time to resolve.

- Days 30 to 60: Flag. Risk register comes together as both the contract terms and the variance findings are reviewed in parallel.

- Days 45 to 90: Act. Recovery work starts as soon as underpayments are confirmed. Renegotiation prep and harmonization decisions extend through the end of the cycle.

After the first cycle, the audit becomes an ongoing process. Best practice is quarterly variance re-analysis and an annual full contract review to catch fee schedule changes that payers push out without notice.

Tools and software for payer contract audits

Three categories of tooling make the audit repeatable at MSO scale.

Contract management and underpayment detection software. A platform like RevFind centralizes every payer contract across every TIN, ingests fee schedules at the CPT and modifier level, and runs continuous variance detection against contracted rates. MSO platforms running multiple acquisitions per year benefit most from this category, because manual variance analysis does not scale past two or three acquisitions.

Healthcare legal counsel with payer contracting experience. The legal review of anti-assignment, change of control, and termination provisions should go to attorneys who specialize in healthcare. Generalist M&A counsel will catch the deal-level issues but may miss the payer-specific terms that determine whether the contract survives close.

Managed care consulting for renegotiation. When renegotiation queues are long, MSO managed care teams often bring in outside consultants who specialize in payer rate negotiations and bring benchmark data from comparable deals. This is especially valuable for the first one or two acquisitions on a new platform, when the MSO has not yet built internal benchmarks.

For a deeper look at how technology supports multi-entity contract management, MD Clarity's guide to fee schedule reimbursement walks through the operating model.

Frequently asked questions about payer contract audits after acquisitions

How do you start a payer contract audit after acquiring a physician practice?

Start by inventorying every payer contract, amendment, and fee schedule at the acquired entity within the first two weeks. The inventory typically reveals missing documents, which sets the agenda for follow-up. Once inventoried, contracts are loaded into a contract management platform, fee schedules digitized at the CPT and modifier level, and a variance analysis run against 12 to 24 months of remit data.

What are the biggest risks in inherited payer contracts?

The three highest-impact risks are anti-assignment clauses where payer consent was not obtained (which can make contracts voidable), persistent underpayments against contracted rates (typically 1 to 3 percent of net patient revenue), and termination provisions with short notice windows that limit the MSO's renegotiation leverage.

Can a buyer assume the acquired practice's payer contracts?

It depends on the deal structure and the contract terms. In a stock purchase, contracts may carry over with change of control consent. In an asset purchase, buyers can decline to assume contracts and instead enroll as a new provider, which avoids inheriting pre-close liabilities. Most commercial payer contracts contain anti-assignment clauses requiring written payer consent on transfer.

How much revenue can an audit recover?

Typical first-cycle audits recover 1 to 3 percent of net patient revenue in underpayments from the prior 12 to 24 months, subject to payer-specific timely filing limits. For a $50 million practice, that translates to $500,000 to $1.5 million in recovered revenue plus the recurring annual benefit of correcting the underlying rate issue going forward.

How often should payer contracts be re-audited?

Variance analysis should run continuously (not as a periodic project), since payers push fee schedule changes regularly. The full contract review (terms, fee schedules, performance benchmarks) should be repeated annually, with additional reviews triggered by any payer-initiated amendment, new value-based care arrangement, or MSO platform acquisition.

What is a fee schedule audit vs. a payer contract audit?

A fee schedule audit reviews whether contracted rates are at or above market for the procedure mix the practice performs. A payer contract audit is broader: it includes fee schedule analysis plus a review of contract terms (assignability, termination, renewal, escalators), payment performance against contracted rates, and operational compliance with contract provisions like timely filing and appeal windows.

Who should run the audit, the MSO or an outside firm?

For the first one or two acquisitions on a new platform, outside consultants with managed care expertise and benchmark data often accelerate the work. For platforms with mature contract management software and an experienced managed care team, the audit becomes a repeatable internal function. Most MSO platforms eventually bring this in-house, since the same team will run audits on every future add-on acquisition.

Make payer contract audits a repeatable capability

A payer contract audit is not a one-time integration project. It is a permanent operating capability that the MSO needs to build, refine, and run on every acquired entity. The platforms that get this right capture the underpayments, renegotiate the bad contracts, and harmonize the inherited agreements faster than their competitors - which is exactly what makes their EBITDA thesis hold up across a roll-up strategy.

MD Clarity helps MSO managed care and revenue cycle teams audit, monitor, and act on payer contracts across every TIN in the platform. See the platform in action or read about how an orthopedics MSO found $10.3 million in underpayments using this exact framework.

FAQs

Get paid in full by bringing clarity to your revenue cycle

Related Posts

Subscribe to the

Healthcare Clarified newsletter

Get the latest insights on RCM and healthcare policy in your inbox