.avif)

.svg)

.svg)

Consolidating payer contracts across a multi-TIN MSO is the strategic work of moving from a patchwork of inherited payer agreements (one or more per acquired entity) to a unified contract structure that delivers platform-scale rates, simplifies reporting, and reduces administrative drag. Most MSO platforms run 5 to 25 tax IDs by the time they hit institutional scale, and the choice of consolidation strategy determines whether the platform actually captures the negotiating leverage its size should command.

This guide is for MSO VPs of managed care, directors of revenue cycle, CFOs, and the private equity operating partners who measure whether RCM integration is translating into margin. It covers why MSOs end up with multiple TINs, the four consolidation strategies and when each fits, the 18-month execution roadmap, and the multi-TIN reporting requirements that keep the platform manageable as it grows.

What does payer contract consolidation mean for a multi-TIN MSO?

Payer contract consolidation across a multi-TIN MSO refers to harmonizing the contracts, rates, and operational terms that govern reimbursement at every tax ID in the platform. The work spans three connected layers:

- Legal structure. Which entity actually holds each payer contract, and whether contracts are master agreements covering all entities, individual agreements per entity, or hybrid umbrella structures.

- Rate harmonization. Whether all entities are reimbursed at the same rate for the same service from the same payer, or whether legacy rates persist by acquired entity.

- Operational integration. Whether claims, credentialing, and remittances flow through standardized workflows or remain entity-specific.

Consolidation is not always the right answer. Sometimes the right move is to keep contracts separate, sometimes to use a clinically integrated network, sometimes to push everything onto the MSO's master TIN. The strategy depends on the platform's specialty mix, geographic footprint, state corporate practice of medicine (CPOM) constraints, and growth plans.

This work sits inside the broader post-acquisition revenue cycle integration playbook, and it almost always follows the payer contract audit work for each acquired entity.

Why do MSOs operate with multiple TINs in the first place?

Most MSO platforms accumulate TINs for one or more of the following reasons.

Corporate practice of medicine (CPOM) laws. Roughly 33 states restrict the corporate practice of medicine, which means lay-owned corporations cannot directly own a physician practice. The standard workaround is the friendly PC model: a professional corporation (PC) owned by a licensed physician retains formal ownership of the medical practice, while the MSO (owned by PE or other corporate capital) provides administrative services. Each friendly PC is its own legal entity with its own TIN.

Serial acquisitions. Each add-on acquisition brings at least one new TIN into the platform. A platform that has closed ten add-on acquisitions almost always has ten or more TINs to manage, since asset purchases typically retain the acquired entity's legal structure to preserve payer contracts and licenses.

Geographic separation. Multi-state MSO platforms often need separate legal entities by state to comply with state licensure, insurance, and corporate practice rules. A 20-state platform might operate 25 to 30 TINs just to satisfy state-level structural requirements.

Joint ventures. Some MSO platforms operate joint ventures with health systems, hospitals, or strategic specialty groups. JVs typically have their own TINs and their own payer contract relationships.

Service line separation. Some platforms separate ASCs, anesthesia groups, imaging centers, and physician practices into different TINs for liability, payer contracting, and tax reasons.

The result is that a single MSO platform reporting to a PE board with one EBITDA number is almost always operating across many TINs with many different payer contracts behind that number.

The four payer contract consolidation strategies

There are four distinct paths an MSO can take to consolidate payer contracts across multiple TINs. Most mature platforms run a hybrid of two or three, not just one.

Strategy 1: Master contract on the MSO TIN

In this approach, the MSO (or a master billing entity within the MSO structure) becomes the single contracted party with each payer. Acquired entities are added as locations or affiliated providers under the master agreement, but the legal contract sits with one TIN.

How it works: The MSO renegotiates with each major payer to move from per-entity contracts to a single master contract. Providers re-credential under the master TIN. All claims bill through that TIN regardless of which acquired practice the patient visited.

When to use: Single-state platforms in non-CPOM states, platforms that have reached enough scale to attract payer interest in a master arrangement, and specialties where payer-side contract teams are willing to consolidate. Most common in dental DSOs and some derm and ophthalmology platforms.

Pros: Cleanest reporting (everything rolls up to one TIN), maximum platform negotiating leverage, lowest administrative overhead.

Cons: Re-credentialing every provider can take 90 to 180 days per payer per provider, NPI and TIN mismatches during the transition can cause claim denials, and many state CPOM laws prevent the MSO from being the contracting party for clinical services.

Strategy 2: Parent-child or umbrella contracts

The umbrella approach keeps individual TINs intact but layers a master rate framework on top. Each acquired entity retains its own TIN and contract, but rates and terms reference a shared parent agreement.

How it works: The MSO negotiates a parent agreement with each payer that establishes master rate methodology, escalators, and renewal terms. Each subsidiary TIN then has a "child" contract that adopts the parent terms while preserving the legal separation between entities.

When to use: Multi-state platforms, mixed-specialty platforms, and platforms still actively acquiring. The umbrella structure preserves flexibility for add-ons while still concentrating negotiating leverage at the parent level.

Pros: Preserves existing TINs (no re-credentialing wave), centralizes rate strategy without forcing legal consolidation, flexible enough to accommodate new acquisitions on consistent terms.

Cons: Some commercial payers refuse to negotiate umbrella structures, particularly Medicare Advantage plans that prefer per-entity contracts. Administratively more complex than a single master contract, since each subsidiary TIN still has its own administrative obligations.

Strategy 3: Soft consolidation through a CIN or IPA

Soft consolidation uses a clinically integrated network (CIN) or independent practice association (IPA) as a contracting vehicle. Practices remain independently owned and contracted, but they negotiate jointly through the network entity.

How it works: The MSO sets up (or affiliates with) a CIN or IPA that meets the clinical integration standards needed to support joint payer contracting under antitrust law. Practices join the network and the network negotiates contracts on their behalf. According to the Milbank Memorial Fund, this is the structure that allows "otherwise independent providers to engage in joint payer contracting without violating antitrust laws that prohibit price fixing."

When to use: Platforms where physician practices want operational autonomy, multi-state platforms with antitrust exposure, and value-based care arrangements where clinical integration is required by the payer anyway.

Pros: Allows joint payer negotiation while preserving practice-level ownership, antitrust-safe when the CIN meets FTC integration standards, supports value-based contracting.

Cons: Requires real clinical integration (not just contractual), including shared protocols, quality measurement, and performance management. Slow and expensive to set up. Less negotiating leverage than a fully consolidated structure.

Strategy 4: Maintain separate TIN contracts

The fourth option is to not consolidate at all. Each acquired entity keeps its existing payer contracts under its existing TIN, and the MSO focuses on operational integration rather than contract harmonization.

How it works: No payer renegotiation required. The MSO's centralized revenue cycle operates each TIN under its own contracts and tracks performance across the platform through reporting tools rather than contract structure.

When to use: Early-stage platforms before scale exists, platforms with specialty divergence where payer mix differs materially across entities, situations where existing contracts are already strong, or short-term post-close periods before broader consolidation begins.

Pros: Zero payer renegotiation cost, fast post-acquisition stability, no claim disruption.

Cons: Forfeits platform negotiating leverage, fragmented reporting, leaves rate disparities across the platform that the next CFO review will challenge.

How to choose the right consolidation strategy

The choice between these four paths depends on five factors.

State CPOM laws. In states with strict CPOM enforcement, the MSO cannot be the contracting party with payers for clinical services. This rules out Strategy 1 in many states and pushes the platform toward parent-child or soft consolidation models. Healthcare counsel familiar with state-specific CPOM enforcement should weigh in early.

Specialty mix. Single-specialty platforms can consolidate more aggressively because the payer fee schedule complexity is more uniform. Multi-specialty platforms often need different strategies for different specialties within the same MSO.

Geographic footprint. A single-state or single-region platform can pursue a master contract more easily than a 20-state platform. Multi-state platforms typically default to umbrella or soft consolidation structures.

Payer market structure. In markets dominated by one or two commercial payers, the MSO has more leverage to push for consolidation and the payer has more reason to accept it. In fragmented markets, separate contracts may persist longer because no single payer is worth the renegotiation effort.

Platform maturity. Early-stage platforms with 2 to 5 acquisitions usually run Strategy 4 (separate contracts) while building out RCM infrastructure. Mid-stage platforms with 5 to 15 acquisitions typically transition to Strategy 2 (parent-child). Mature platforms with 15+ entities often pursue Strategy 1 or 3 depending on CPOM constraints.

The right answer is almost never one strategy across the entire platform. Most mature MSOs run a hybrid: a master contract with the dominant local commercial payer, an umbrella structure with national payers, a CIN for value-based contracts, and separate contracts for niche payers that aren't worth the renegotiation effort.

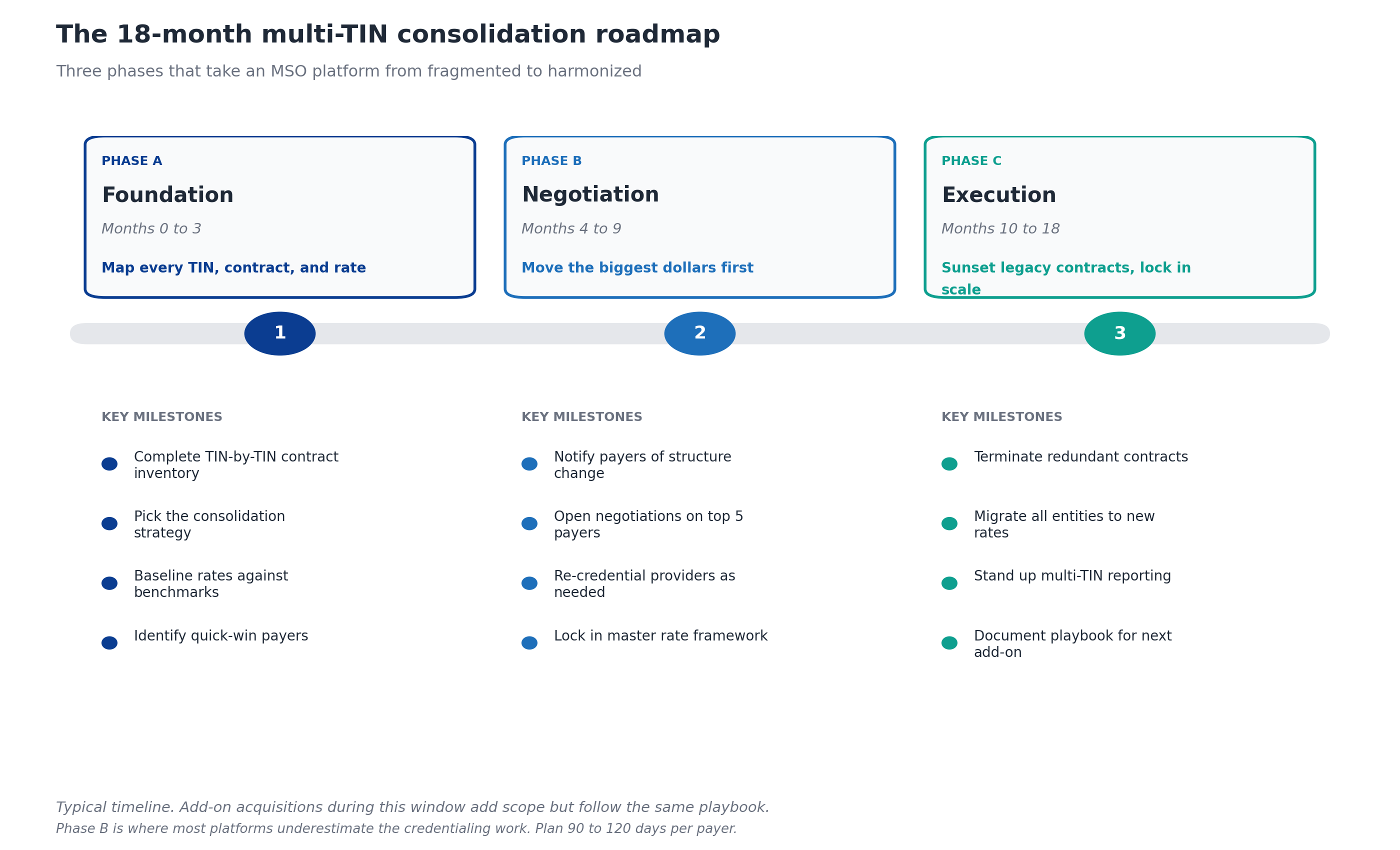

The 18-month multi-TIN consolidation roadmap

Once the strategy is chosen, execution typically takes 12 to 24 months for a platform's existing TINs (longer if add-on acquisitions are happening during the same window). The roadmap breaks into three phases.

Phase A: Foundation (Months 0 to 3)

The foundation phase establishes what consolidation is actually working with. Three deliverables matter:

- Complete TIN-by-TIN contract inventory. Every active payer contract at every TIN in the platform, including amendments, fee schedules, and historical rate changes. This often surfaces 10 to 20 percent more contracts than the platform thought it had.

- Strategic decision on consolidation approach. Which of the four strategies (or hybrid combinations) applies to which payer relationships, with rationale documented for the board.

- Rate baseline against benchmarks. Where do rates sit at each TIN versus market benchmarks? Which TINs have the best rates? Which payers have the most variance across TINs?

The foundation phase also includes selecting the contract management technology that will host the consolidated rates and run continuous performance monitoring. MD Clarity's guide to healthcare contracts walks through what to look for.

Phase B: Negotiation (Months 4 to 9)

Phase B is the dollar-impact phase. The managed care team opens negotiations on the payers that matter most.

- Notify payers of structure change. Every commercial payer with an anti-assignment or change-of-control clause needs formal written notice. Counsel should review the notice language to preserve the platform's negotiating posture.

- Open negotiations on top 5 payers by revenue. Concentrate effort where the dollars are. Most MSO platforms find that 5 to 8 payers account for 70 to 80 percent of net patient revenue, and those are the contracts that justify executive bandwidth.

- Re-credential providers as needed. If the strategy involves moving providers onto a new master TIN, credentialing has to start in Phase B. HFMA notes that payer leverage in negotiations is enhanced by consolidation, but the leverage doesn't help if providers aren't credentialed when the new contract goes live.

- Lock in master rate framework. Even if some payers refuse the consolidation structure, get the master rate framework documented and adopted across whichever payers will accept it.

This is also the phase where unexpected payer pushback surfaces. Some payers will refuse to extend the MSO's best rates to acquired entities. Some will use the consolidation moment to push for unfavorable contract terms in exchange. The managed care team needs leverage and patience, and ideally a credible alternative (going out of network in markets where the platform has scale).

Phase C: Execution (Months 10 to 18)

The execution phase locks everything in.

- Terminate redundant contracts. Once new contracts are live, the inherited legacy contracts at acquired entities get formally terminated per their notice provisions. This is more administrative work than it sounds, since termination has to happen contract-by-contract with proper notice.

- Migrate all entities to new rates. Billing systems, fee schedules, and remittance reconciliation move to the consolidated framework. This is where claim denials often spike if migration is rushed.

- Stand up multi-TIN reporting. Net revenue, EBITDA, payer mix, denial rates, and underpayment exposure all need to roll up to platform-level reporting while remaining drillable to the TIN, specialty, site, and provider level.

- Document the playbook. The next acquisition that joins the platform should follow a documented integration playbook, not repeat the discovery work. This is what makes consolidation a repeatable capability rather than a one-time project.

What multi-TIN reporting requires

Multi-TIN reporting is what separates well-run MSO platforms from struggling ones. The CFO and PE board want to see the platform consolidated, but the operational teams need to see entity-level performance to catch problems early.

The reporting structure needs to support three levels of view:

Platform level. Aggregate net revenue, EBITDA, denial rate, days in A/R, and underpayment exposure rolled up across every TIN. This is what goes to the PE board.

TIN level. The same metrics broken out by tax ID, with comparisons against platform benchmarks. This is what the central revenue cycle leadership uses to spot integration drift in acquired entities.

Drill-down level. Below the TIN, the team needs to see performance by specialty, site, provider, payer, and CPT. This is where the underlying issues (a specific payer underpaying a specific procedure at a specific site) actually surface.

This reporting layer is also where the advantage of multi-TIN visibility compounds. The MSO can see which payer is underpaying which specialty across which TINs, route recovery work to the right team, and use the aggregate findings as leverage in renegotiations.

Common pitfalls in multi-TIN contract consolidation

After watching MSO platforms run this play, certain mistakes show up repeatedly.

Over-consolidating before scale exists. Pushing every acquired entity onto a master contract before the platform has enough volume to justify the renegotiation effort. Payers will agree to the consolidation but not to better rates, leaving the platform with the same rates plus the administrative cost of a single contract.

Underestimating credentialing. Moving providers onto a new TIN means re-credentialing every provider with every payer. This routinely takes longer than expected and is one of the most common reasons consolidation timelines slip.

Ignoring CPOM constraints. Pushing a Strategy 1 master contract in a state with strict CPOM enforcement. The legal exposure usually surfaces when a regulator or competing PC files a complaint, and unwinding the structure is expensive.

Failing to model the rate exposure. Some acquired entities have better rates than the MSO platform for specific procedure families. Consolidating without modeling this carefully can actually destroy revenue by replacing strong contracts with weaker master agreements.

Treating the project as legal work only. Contract consolidation is operational work that requires legal, managed care, revenue cycle, and credentialing teams working together. Platforms that treat it as a legal initiative miss the operational complexity.

Skipping the playbook. Each acquisition repeats the discovery, decision, and execution work as if it were the first. Mature platforms build a documented consolidation playbook so the work compounds rather than starts over.

Technology requirements for multi-TIN contract management

Three categories of technology make multi-TIN consolidation manageable at scale.

Contract management with multi-TIN architecture. The platform needs to support multiple TINs natively, with the ability to ingest different fee schedule formats, track parent-child relationships, and run variance detection across every TIN simultaneously. Most generalist contract management tools struggle here because they were built for single-entity hospitals or single-TIN groups.

Underpayment detection across the platform. Once contracts are loaded, the same engine should be detecting variances on every TIN against the right fee schedule. This is where platforms like RevFind add the most value, because the variance findings inform both recovery work and renegotiation strategy.

Reporting that rolls up and drills down. Reporting infrastructure that can present platform-level totals to the board while supporting drill-downs to specialty, site, provider, and payer for the operating teams. For a deeper look at the operating model, MD Clarity's guide to payer contract management for MSOs walks through the technology stack and integration points.

Frequently asked questions about multi-TIN payer contract consolidation

What is multi-TIN payer contract consolidation?

Multi-TIN payer contract consolidation is the process of moving a healthcare MSO platform from a patchwork of inherited payer contracts (typically one or more per acquired entity) to a unified contract structure that delivers consistent rates, simplified reporting, and platform-scale negotiating leverage. The work spans legal structure, rate harmonization, and operational integration.

Why do MSOs have multiple TINs?

MSOs accumulate multiple TINs because of state corporate practice of medicine (CPOM) laws (which require separate physician-owned PCs), serial acquisitions (each adding a new legal entity), multi-state operations (each state requiring its own entity), joint ventures, and service line separation. Most institutional-scale MSOs operate between 5 and 25 TINs.

Can payer contracts be transferred between TINs?

Most commercial payer contracts cannot simply be transferred. They contain anti-assignment clauses requiring written payer consent on change of control. The standard playbook is to notify payers per contractual requirements, identify which contracts can be terminated and rolled onto the MSO master contract or umbrella structure, and negotiate the new arrangement directly rather than rely on transfer.

How long does multi-TIN contract consolidation take?

A typical consolidation timeline for an existing MSO platform runs 12 to 24 months, broken into a three-month foundation phase, a six-month negotiation phase with top payers, and a 9 to 12 month execution phase. Platforms actively acquiring during this window often run consolidation as a continuous capability rather than a one-time project.

What is a friendly PC model and how does it affect contract consolidation?

A friendly PC model is the standard MSO structure used in states with corporate practice of medicine (CPOM) restrictions. A professional corporation owned by a licensed physician retains formal ownership of the medical practice, while the MSO provides administrative services. Because the PC (not the MSO) is the contracting entity with payers, the friendly PC model limits which consolidation strategies are available and often pushes platforms toward umbrella structures or soft consolidation through CINs.

What is the difference between a CIN and an IPA for payer contracting?

A clinically integrated network (CIN) is an organization of otherwise-independent providers that have created sufficient clinical integration (shared protocols, quality measurement, performance management) to support joint payer contracting under antitrust law. An independent practice association (IPA) is a legal entity formed by independent practices to jointly contract with payers, typically with less clinical integration than a CIN. Both can serve as payer contracting vehicles for MSO platforms that need joint negotiation without consolidated ownership.

How much can consolidation increase reimbursement rates?

Rate improvement varies widely by payer market, specialty, and consolidation strategy, but mid-single-digit to low-double-digit rate improvements are common for top commercial payers when an MSO platform moves from per-entity contracts to a master or umbrella structure. The biggest gains usually come from harmonizing acquired entities upward to the MSO's best existing rate rather than from pure new-rate negotiations.

What goes wrong most often in multi-TIN consolidation?

The three most common failure modes are: underestimating credentialing timelines (which delays the new contract going live), over-consolidating before the platform has enough scale to justify the effort, and ignoring state CPOM constraints that limit which consolidation paths are legally available.

Make consolidation a repeatable capability

Multi-TIN contract consolidation is not a one-time integration project. It is a continuous operating capability that mature MSO platforms build, refine, and apply to every new acquisition. The platforms that get this right capture platform-scale negotiating leverage, simplify their reporting, and turn each add-on acquisition into a faster integration than the one before.

MD Clarity helps MSO managed care and revenue cycle teams manage payer contracts across every TIN in the platform, detect underpayments at scale, and report performance from platform level down to the CPT level. See the platform in action or read about how an orthopedics MSO found $10.3 million in underpayments by consolidating contract management across its platform.

FAQs

Get paid in full by bringing clarity to your revenue cycle

Related Posts

Subscribe to the

Healthcare Clarified newsletter

Get the latest insights on RCM and healthcare policy in your inbox