.avif)

.svg)

.svg)

Revenue cycle red flags in healthcare M&A due diligence are operational, contractual, and financial warning signs in a target's billing and collections operation that signal either inflated current EBITDA, hidden integration costs, or fundamental risks to post-close performance. A disciplined RCM diligence process identifies these red flags before close, quantifies their dollar impact, and routes each one to the right outcome: walk away, adjust the purchase price, build into integration planning, or accept and move on. Most acquired practices surface between 8 and 15 red flags during diligence. None of them are reasons not to do the deal on their own; together, they reshape the deal terms and the synergy thesis.

This guide is for PE associates and operating partners doing diligence, investment bankers advising on healthcare deals, MSO platform CFOs and corporate development teams evaluating add-on targets, and the quality of earnings (QoE) providers who support these transactions. It covers what RCM red flags actually are, the six categories of red flags to screen for, the specific KPI thresholds that mark concern vs. dealbreaker, how findings translate to price adjustments and integration plans, and the common mistakes that leave buyers exposed post-close.

Why revenue cycle diligence is often underweighted in healthcare M&A

Most healthcare M&A diligence concentrates effort on three areas: financial normalization (verifying EBITDA, scrutinizing add-backs), legal and regulatory review (HIPAA, Stark Law, anti-kickback), and clinical operations. Revenue cycle gets folded into the financial review without the depth the topic warrants.

This is a structural mistake. As analysts have noted, RCM can dictate up to 40 percent of operational efficiency in a healthcare organization, and seemingly minor billing and collections issues directly impact profitability and long-term viability. Market research shows that financial distress or reimbursement variability influenced more than 40 percent of provider-side M&A transactions in 2025.

Three dynamics explain why RCM diligence falls through the cracks:

The data is hard to access. Payer contracts are scattered across shared drives and paper files. Remit data lives inside the practice management system in formats that don't easily export. Denial reports often don't exist. Independent practices typically have no continuous variance detection, so the data buyers want to see often hasn't been compiled.

The expertise is specialized. Generalist M&A diligence teams can read financial statements but often miss the nuances of payer contract terms, fee schedule methodology, or denial workflow. As healthcare attorneys at Cranfill Sumner observe, buyers are now conducting deeper due diligence than ever before, but the deeper review requires healthcare-specific expertise that not every transaction team has.

The timeline is short. Competitive auction processes compress diligence into 4 to 8 weeks. Within that window, RCM analysis competes with financial QoE, legal review, clinical assessment, and commercial diligence. The teams that miss RCM red flags are usually the ones that ran out of time, not the ones that didn't know what to look for.

The buyers who do this work well treat RCM diligence as its own work stream, staffed by healthcare-specialized analysts, with technology that ingests contracts and remits quickly enough to support the timeline. The output is a documented red flag inventory tied to dollar impact, which becomes the foundation of both purchase price negotiation and the integration plan after close.

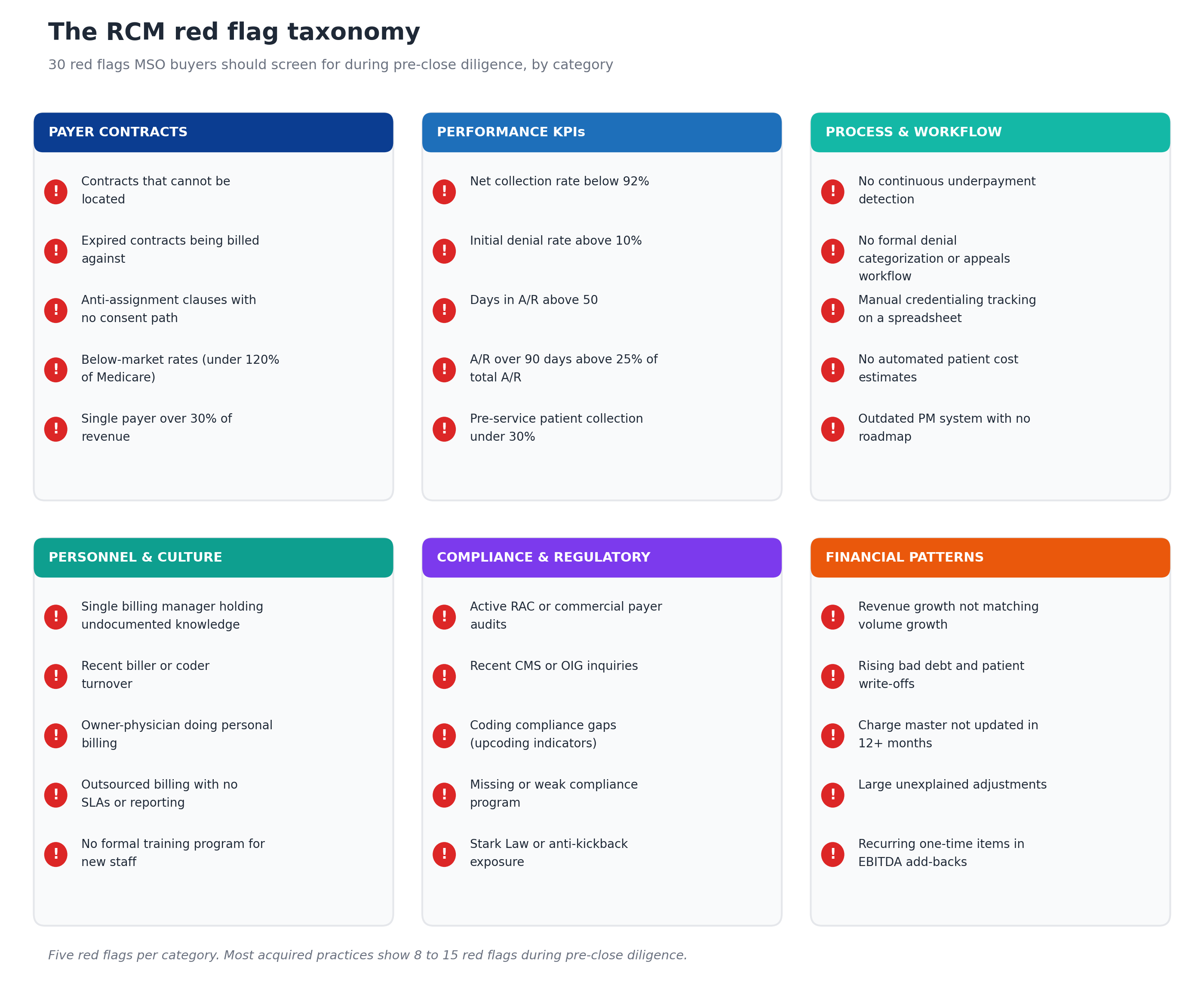

The six categories of RCM red flags

Every RCM diligence finding falls into one of six categories. The categories matter because they drive different deal outcomes: contract findings often support purchase price adjustments, performance findings inform the synergy thesis, compliance findings shape rep and warranty negotiations, and process findings drive the integration plan.

The taxonomy is meant to be exhaustive but not equally weighted. Some red flags are dealbreakers (active fraud investigations, severe compliance gaps). Others are standard integration work (aged A/R in the 60 to 90 day bucket, manual denial workflow). The severity matrix later in this guide explains how to weight each finding.

Category 1: Payer contract red flags

Payer contracts produce more diligence findings than any other category because they are simultaneously the highest-impact area for value (rates determine reimbursement) and the area with the worst documentation hygiene at most targets.

Contracts that cannot be located. When the target cannot produce every active payer contract, the rate methodology and contract terms are uncertain. The buyer is acquiring revenue subject to contracts they have not read. This finding alone can warrant escrow provisions tied to post-close contract discovery.

Expired contracts being billed against. Some practices continue billing under contracts that have technically expired, relying on auto-renewal provisions that the payer may or may not honor. The risk is that the payer reprices to default rates retroactively or terminates the relationship.

Anti-assignment clauses with no consent path. Most commercial payer contracts require written payer consent on change of control. Contracts with strict anti-assignment language and no documented consent path may be voidable post-transaction, which can crater the synergy thesis if the contracts represent the practice's best rates.

Below-market rates. Commercial contracts priced below 120 percent of Medicare for routine codes (or below 150 percent for procedural specialties) are well below typical market levels. This is both a red flag (the practice is leaving money on the table) and an opportunity (the rates can be renegotiated post-close, supporting the synergy thesis).

Single payer over 30 percent of revenue. Payer concentration above 30 percent creates significant risk: if the dominant payer changes terms, terminates the contract, or shifts members to a different product, revenue collapses. Industry research consistently identifies customer concentration above 20 percent as a generic M&A red flag, and the threshold is similar for healthcare payer concentration.

Category 2: Performance KPI red flags

KPI thresholds are the most quantifiable red flags. They translate directly to dollar amounts the buyer can model into the deal.

Each threshold has been calibrated against industry benchmarks from HFMA, MGMA, Experian Health, and Kodiak Solutions.

Net collection rate below 92 percent. Healthy practices collect 95 to 98 percent of allowed amounts. Practices below 92 percent are losing real revenue to write-offs, often because they lack continuous variance detection or have weak denial workflows.

Initial denial rate above 10 percent. Industry research shows that initial claim denial rates have climbed steadily, with denials reaching nearly 12 percent of submitted claims in 2024. Practices above 10 percent are typically dealing with payer-specific operational issues that the buyer will inherit.

Days in A/R above 50. Healthy practices collect within 30 to 40 days of service. Above 50 days, working capital is tied up and collection probability is dropping. Industry analysis consistently identifies A/R days outstanding above 60 as a major red flag.

A/R over 90 days above 25 percent of total A/R. Healthy practices hold less than 18 percent of A/R in the 90-plus bucket. Above 25 percent, collection probability falls sharply and the practice is heading toward write-offs.

Cost to collect above 6 percent. Healthy revenue cycle operations run at 2 to 4 percent of collections. Above 6 percent indicates structural inefficiency that will require operational change to fix.

Pre-service patient collection below 30 percent. Healthy practices collect more than 70 percent of patient responsibility at or before the visit. Below 30 percent, patient bad debt accumulates and the practice is exposed to the collection rate decline the industry has been seeing.

The KPI gauges in Figure 2 anchor the diligence team's quantitative review. When a target's metrics fall into red zones, the buyer should request explanations, model the recovery potential under MSO platform standards, and factor the gap into either the synergy thesis or the price negotiation.

Category 3: Process & workflow red flags

Process red flags identify operational gaps that will require integration effort to fix. Each one points to a specific workflow that needs MSO platform standards applied post-close.

No continuous underpayment detection. Most independent practices have no system that compares paid amounts against contracted rates at the CPT level. Industry estimates put healthcare underpayments at 1 to 3 percent of net patient revenue annually, accumulating silently. The absence of detection is itself the red flag.

No formal denial categorization or appeals workflow. Practices without standardized denial categorization (by payer, by denial code, by root cause) and without tracked appeals processes are losing recoverable denials to time. The cost to rework a single denial ranges from $25 to $181, and low-dollar denials routinely get abandoned because the rework economics don't pencil out.

Manual credentialing tracking on a spreadsheet. Credentialing under multiple payers across multiple providers requires tracking that scales. Spreadsheet-based tracking signals that the practice has likely missed expirations, has gaps the management team isn't aware of, and lacks the data the MSO will need for Day 1 integration.

No automated patient cost estimates. Federal price transparency rules now require Good Faith Estimates for self-pay patients, and patient financial expectations require accurate estimates before service. Practices without automated estimation are exposed on both the compliance side and the patient collection side.

Outdated PM system with no roadmap. Practice management systems older than 7 to 10 years often lack the integration points needed for centralized MSO operations. The migration cost (typically $50,000 to $250,000 per location depending on complexity) and the migration risk (60 to 90 days of potential cash disruption) are both meaningful and need to factor into the integration plan.

Category 4: Personnel & culture red flags

Personnel red flags are the most underestimated category in RCM diligence because they don't show up in financial statements. They show up two to six months post-close when key people leave and undocumented institutional knowledge disappears.

Single billing manager holding undocumented knowledge. Most independent practices have one person who knows where the payer relationships are, which denial codes need supplementary documentation, and which providers code below their actual work. Losing that person post-close costs more than most retention packages would have cost.

Recent biller or coder turnover. Turnover in the 6 to 12 months before sale often signals operational stress that the financial statements haven't yet caught up to. Recent departures usually mean the remaining staff have been working around problems that the buyer will inherit.

Owner-physician doing personal billing. When the selling physician handles their own billing (or closely oversees it without delegating), the practice has no operating model independent of that person. Post-close, when the physician steps back, the billing falls apart unless the MSO has built a replacement function first.

Outsourced billing with no SLAs or reporting. Outsourced billing arrangements with no service level agreements, no monthly performance reporting, and no escalation paths typically perform poorly. The buyer inherits the outsourcing contract along with the practice and often discovers that the relationship needs to be replaced.

No formal training program for new staff. Practices without documented training programs cannot scale and cannot weather turnover. The training gap shows up as denials and collection issues when staff turn over post-close.

Category 5: Compliance & regulatory red flags

Compliance red flags carry the highest potential severity because regulatory exposure can survive the transaction and bind the buyer post-close.

Active RAC or commercial payer audits. Recovery Audit Contractor (RAC) audits or commercial payer audits in progress represent contingent liabilities that could materialize as repayment obligations. Buyers need to size the exposure and require the seller to either resolve before close or escrow against the potential.

Recent CMS or OIG inquiries. Government inquiries (CMS recoupment notices, OIG investigations) represent more serious exposure than commercial audits. Active investigations should pause the deal until they resolve or until the buyer has reviewed the underlying facts.

Coding compliance gaps. Patterns suggesting upcoding (unusually high distribution of high-complexity codes, modifier 25 attached to most E&M visits, inconsistent coding within a practice) are visible to auditors and can trigger lookback liabilities. Compliance counsel needs to review coding patterns during diligence, not after.

Missing or weak compliance program. Healthcare compliance programs typically include written policies, designated compliance officers, training requirements, and audit procedures. Practices without documented compliance programs are exposed to OIG enforcement under the False Claims Act and to commercial payer audits.

Stark Law or anti-kickback exposure. Physician practices with referral relationships, equipment leasing arrangements with referring providers, or unusual investor structures may have Stark Law or anti-kickback exposure. Healthcare counsel review is essential and the findings can change the deal.

Category 6: Financial pattern red flags

Financial pattern red flags surface in the financial QoE work but warrant separate attention because they often point to RCM operational issues underneath.

Revenue growth not matching volume growth. If patient volume is flat but revenue is growing 8 percent per year, the practice is either getting rate increases (good) or charging more aggressively (a red flag). If revenue is growing slower than volume, the practice has rate compression that the buyer will inherit.

Rising bad debt and patient write-offs. Patient bad debt that has been growing year over year signals a deteriorating patient collection process. The buyer should expect the trend to continue absent operational change.

Charge master not updated in 12+ months. Charge masters require regular updates to reflect current CPT codes, pricing strategy, and lesser-of-charges contract dynamics. An outdated charge master often correlates with broader operational neglect.

Large unexplained adjustments. Practices with large monthly or quarterly adjustments that aren't clearly categorized (e.g., contractual vs. bad debt vs. courtesy) signal weak revenue recognition discipline. As QoE providers consistently note, poor documentation to support EBITDA add-backs is a common red flag.

Recurring one-time items in EBITDA add-backs. When a target presents EBITDA with significant add-backs labeled as "one-time" but the same category appears year over year, the buyer should treat those items as recurring expenses, not add-backs. This often reduces the deal-relevant EBITDA by 5 to 15 percent.

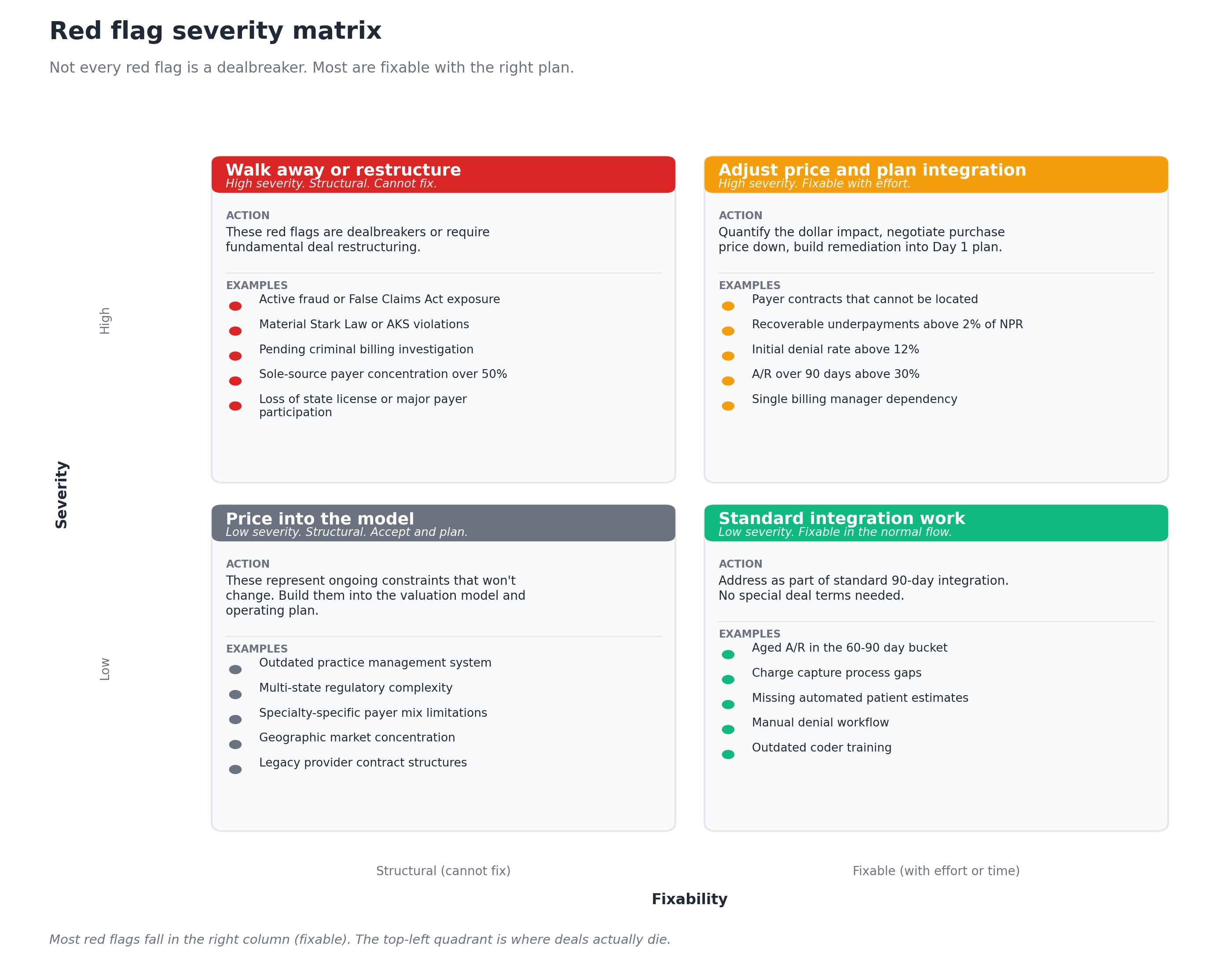

How red flags translate to deal terms

Not every red flag is a dealbreaker. The right response depends on the severity of the issue and the fixability.

Walk away or restructure. High-severity structural issues. Active fraud or False Claims Act exposure, material Stark Law violations, pending criminal billing investigations, sole-source payer concentration over 50 percent, and loss of state licensure are dealbreakers or require fundamental deal restructuring. These rarely surface in cleaned-up sale processes but appear often enough in distressed transactions that buyers need to screen for them.

Adjust price and plan integration. High-severity issues that are fixable with effort. Payer contracts that cannot be located, recoverable underpayments above 2 percent of NPR, initial denial rates above 12 percent, A/R over 90 days above 30 percent, and single billing manager dependency all fit here. The right response is to quantify the dollar impact, negotiate the purchase price down by some portion of the recoverable value, and build remediation into the Day 1 integration plan.

Price into the model. Low-severity structural issues that won't change post-close. Outdated practice management systems, multi-state regulatory complexity, specialty-specific payer mix limitations, geographic market concentration, and legacy provider contract structures all fit here. The buyer accepts the constraint and builds it into the valuation model and operating plan.

Standard integration work. Low-severity issues that fit within normal post-close integration. Aged A/R in the 60 to 90 day bucket, charge capture process gaps, missing automated patient estimates, manual denial workflow, and outdated coder training all get addressed as part of the standard 90-day integration. No special deal terms are needed.

The single most common mistake is treating every red flag as a dealbreaker (creating diligence paralysis) or treating every red flag as standard integration work (which under-prices the asset and leaves money on the table at close). The severity matrix forces deliberate categorization for each finding.

How to surface red flags during diligence

A disciplined RCM diligence process runs four parallel workstreams over a typical 4 to 8 week diligence window.

Workstream 1: Contract inventory and audit. Request every payer contract, amendment, and fee schedule from the target. Inventory what exists, identify what's missing, and load the contracts into a contract management platform for analysis. The payer contract audit methodology covers this work in detail.

Workstream 2: KPI baselining. Request 24 months of remits and billing data. Calculate net collection rate, initial denial rate, days in A/R, A/R over 90 days, cost to collect, and pre-service collection rate. Compare against the threshold table in Figure 2 and document where the target sits in each gauge.

Workstream 3: Process documentation. Interview the billing manager, the credentialing lead, the lead coder, and any consultants supporting the function. Walk through the workflows for billing, denial management, patient collections, and credentialing. Document where the processes are formal vs. ad hoc.

Workstream 4: Compliance review. Counsel reviews the compliance program documentation, payer audit history, and any open inquiries. Coding consultants sample claims for compliance patterns. Healthcare counsel reviews payer contracts for Stark Law and anti-kickback exposure in any referral relationships.

Each workstream produces findings that get categorized using the taxonomy in Figure 1 and severity-rated using the matrix in Figure 3. The final output is a red flag register that supports both deal negotiation and post-close integration planning.

For the full operational playbook that runs after diligence completes, see the post-acquisition revenue cycle integration framework and the 90-day RCM integration checklist.

Common mistakes in RCM diligence

After watching many healthcare M&A processes, certain mistakes recur.

Treating RCM as a sub-workstream of financial QoE. Financial QoE teams verify revenue and normalize EBITDA. They don't typically read payer contracts, audit fee schedules, or interview billing managers. When RCM is folded into QoE, the depth gets lost. Mature buyers staff RCM diligence separately.

Skipping the contract audit because the target says contracts aren't available. "We can't get you all the contracts" is itself a finding. The contracts the buyer cannot read are contracts the buyer is acquiring blind. Some level of contract review is non-negotiable.

Assuming KPI improvements will come automatically post-close. When a target has below-benchmark KPIs, buyers sometimes assume their integration team will fix the gaps post-close and underwrite the synergy at full value. The reality is that gaps require workflow change, technology deployment, and time. Realistic underwriting assumes 50 to 70 percent of the theoretical gap is captured in the first 18 months.

Underweighting personnel risk. The financial statements don't show that the billing manager is the only person who knows how the practice gets paid. Personnel diligence requires actual interviews with the operational team, not just the seller's senior leadership.

Letting the timeline compress out depth. Competitive auctions create pressure to truncate diligence. Buyers who consistently win on price (without overpaying) usually do so by doing deeper RCM work in less time, supported by technology that ingests contracts and remits quickly enough to keep pace.

Failing to convert findings into deal terms. A red flag inventory that doesn't translate into specific purchase price adjustments, escrow provisions, working capital adjustments, or rep and warranty negotiations is a wasted analysis. The findings need to drive the deal, not just inform it.

Technology that accelerates RCM diligence

Three technology categories make RCM diligence work in the compressed timelines that healthcare M&A typically allows.

Contract management with CPT-level fee schedules. The diligence team needs to ingest every payer contract and every fee schedule from the target into a single system within days, not weeks. The contracts have to be searchable, the rates have to be comparable at the CPT level, and the variance against benchmarks has to be quantifiable.

Underpayment detection at scale. Once contracts and remits are loaded, the variance analysis surfaces underpayments in days. The findings translate directly to recoverable revenue estimates that support the synergy thesis or the price negotiation. MD Clarity's RevFind is consistently positioned as a leader in underpayment detection software for multi-entity MSO platforms and add-on diligence specifically because it scales to handle multiple acquisitions in parallel.

Market and platform-best benchmarking. Knowing whether the target's rates are competitive requires reference data. MD Clarity's Payer Benchmarking makes payer transparency files usable as a market benchmarking source, ingesting the federally mandated machine-readable files and standardizing them into formats that diligence teams can compare against the target's contracts. This is what supports the assessment of whether the target has below-market rates that the MSO can renegotiate post-close.

For the broader operating model that connects diligence to post-close execution, MD Clarity's guide to payer contract management for MSOs walks through the integration points.

Frequently asked questions about RCM red flags in healthcare M&A

What are the most common revenue cycle red flags in healthcare M&A?

The most common red flags in any diligence process include payer contracts that cannot be located, recoverable payer underpayments running 1 to 3 percent of net patient revenue, denial rates above 10 percent, A/R over 90 days exceeding 25 percent of total A/R, single billing manager dependency, and patient collection rates below 30 percent pre-service. Most acquired practices show 8 to 15 red flags across the 30-flag taxonomy.

Which RCM red flags are actual dealbreakers?

Active fraud or False Claims Act exposure, material Stark Law or anti-kickback violations, pending criminal billing investigations, sole-source payer concentration over 50 percent, and loss of state license or major payer participation are typically dealbreakers or require fundamental deal restructuring. Most other red flags are fixable with the right purchase price adjustment and integration plan.

How long should RCM diligence take?

Comprehensive RCM diligence typically runs 4 to 6 weeks within a broader 8 to 12 week diligence process. The contract review and KPI baselining each take 10 to 14 days. Process documentation and compliance review run in parallel. Technology that ingests contracts and remits quickly is critical because the timeline rarely allows for manual analysis at scale.

What KPIs should buyers focus on during RCM diligence?

The six KPIs that matter most are net collection rate (healthy above 95 percent), initial denial rate (healthy below 5 percent), days in A/R (healthy below 40), A/R over 90 days (healthy below 18 percent of total A/R), cost to collect (healthy below 4 percent), and pre-service patient collection rate (healthy above 70 percent). Each metric has a clear threshold where performance crosses from healthy into concerning.

How do RCM red flags translate to purchase price adjustments?

For high-severity, fixable red flags, the buyer quantifies the recoverable dollar value, applies a multiple consistent with the deal multiple, and negotiates the purchase price down by some portion of the result. For example, $500K of identified recoverable underpayments at a 10x multiple translates to a $5M valuation reduction, often negotiated down to a $2.5M to $3.5M adjustment to reflect the recovery work the buyer will perform. Findings can also support escrow provisions, working capital adjustments, or specific rep and warranty terms.

Should the buyer or the seller run the RCM diligence?

Buyers should conduct independent RCM diligence even when the seller provides their own QoE work. As MSMS notes regarding third-party financial due diligence, independent diligence is essential because seller-prepared analyses naturally favor the seller's interpretation. Buyer-side diligence catches issues that seller-side analysis misses.

How does RCM diligence connect to integration planning?

The red flag register from diligence directly becomes the foundation of the Day 1 integration plan. Each high-severity, fixable red flag gets assigned to a workstream lead, a remediation timeline, and a measurable target. The 90-day RCM integration checklist walks through how this transition works in practice.

What technology supports RCM diligence?

Three technology categories matter: contract management with CPT-level fee schedule ingestion, underpayment detection that runs variance analysis at scale, and market benchmarking that compares the target's rates against payer transparency file data. These together let a diligence team complete in days work that would take weeks manually, which is critical in competitive auction timelines.

How many red flags is too many?

Most acquired practices surface 8 to 15 red flags during diligence, which is normal and manageable. Practices showing 20 or more red flags often have systemic operational issues that exceed the buyer's appetite for remediation work. The pattern of red flags matters more than the count: 12 red flags concentrated in one category (e.g., compliance) is more concerning than 12 spread across all six categories.

Make RCM diligence a repeatable platform capability

The MSO platforms that consistently close add-on acquisitions on favorable terms are the ones whose RCM diligence runs as a repeatable platform capability, not a fresh project for every deal. The taxonomy, the KPI thresholds, the severity matrix, and the integration playbook all carry forward from one acquisition to the next, which compresses diligence timelines and sharpens the synergy thesis on every successive deal.

MD Clarity helps MSO corporate development, managed care, and revenue cycle teams execute pre-close diligence, quantify red flag dollar impact, and translate findings into the post-close integration plan. Request a demo or read about how an orthopedics MSO found $10.3 million in underpayments by applying this approach.

FAQs

Get paid in full by bringing clarity to your revenue cycle

Related Posts

.avif)

Subscribe to the

Healthcare Clarified newsletter

Get the latest insights on RCM and healthcare policy in your inbox