.avif)

.svg)

.svg)

De novo practice launches and add-on acquisitions both end in the same place (a fully integrated practice operating on MSO platform standards), but the paths to get there require completely different RCM playbooks. A de novo launch starts with a blank slate, no payer contracts, no patient base, and 9 to 18 months of negative cash flow before breakeven. An add-on acquisition starts with inherited operations, existing payer relationships, a working patient base, and positive cash flow from Day 1 (assuming integration goes well). The teams, technology, timelines, and risk profiles for these two growth strategies are not interchangeable.

This guide is for MSO platform CEOs, COOs, CFOs, and corporate development leaders weighing how to grow the platform, plus the revenue cycle and managed care leaders who have to execute whichever path the organization picks. It covers the structural differences between the two approaches, where they diverge on payer contracting, credentialing, technology, and cash flow, and the framework for deciding which path fits which situation.

What is the difference between de novo and add-on RCM integration?

A de novo practice launch is the greenfield development of a new clinical operation from scratch. The MSO designs the site, hires the providers, builds the payer contracts, credentials the team, deploys the technology stack, and operates the practice. There is no prior entity to integrate. The integration work is really a build, not an integration.

An add-on acquisition is the purchase of an existing practice that gets folded into the MSO platform. The MSO inherits everything: the prior owner's payer contracts, fee schedules, billing workflows, denial backlogs, credentialing files, accounts receivable, technology stack, staff, and patient base. The integration work is about preserving what works, consolidating what doesn't, and bringing the acquired entity onto MSO platform standards over 12 to 18 months.

The same MSO platform often runs both strategies simultaneously. De novo is the entry vehicle into new geographies or specialties where no acquirable targets exist at reasonable prices. Add-on is the scaling vehicle within geographies where the MSO already has presence and competing buyers have not yet consolidated the available practices.

This article focuses on the RCM dimension of the comparison. For the broader add-on integration framework, see the post-acquisition revenue cycle integration playbook, and for the operational sequencing of add-on work specifically, see the 90-day RCM integration checklist.

The strategic context: when MSO platforms use each path

PE-backed MSO platforms typically pick growth strategies based on three factors: target availability, capital constraints, and the speed-to-scale thesis.

Target availability. When functional practices are available at reasonable prices, add-on is usually preferred because immediate revenue beats waiting 9 to 18 months for de novo ramp. Many specialty markets (dermatology, orthopedics, GI, ophthalmology) have seen consolidation accelerate, with KPMG reporting that 76 percent of healthcare and life sciences executives expect more M&A activity than the prior year. In saturated markets where competitors have already bought the available targets, de novo becomes the only path.

Capital constraints. Add-on cash flow funds itself from Day 1. De novo requires 9 to 18 months of pre-funded operating expenses, capital that compounds against the PE sponsor's hurdle rate without producing returns during the build period. Platforms with constrained capital lean add-on; platforms with substantial dry powder can afford de novo.

Speed-to-scale thesis. Some PE theses depend on rapid platform scale to support multiple expansion at exit. Add-on delivers scale faster because the revenue is immediate. De novo can deliver scale at lower per-unit cost but on a slower timeline.

Mature platforms typically run both strategies in parallel. The corporate development team evaluates each opportunity against both lenses: "is this market better served by buying or building?" The right answer varies by market.

The dimension-by-dimension comparison

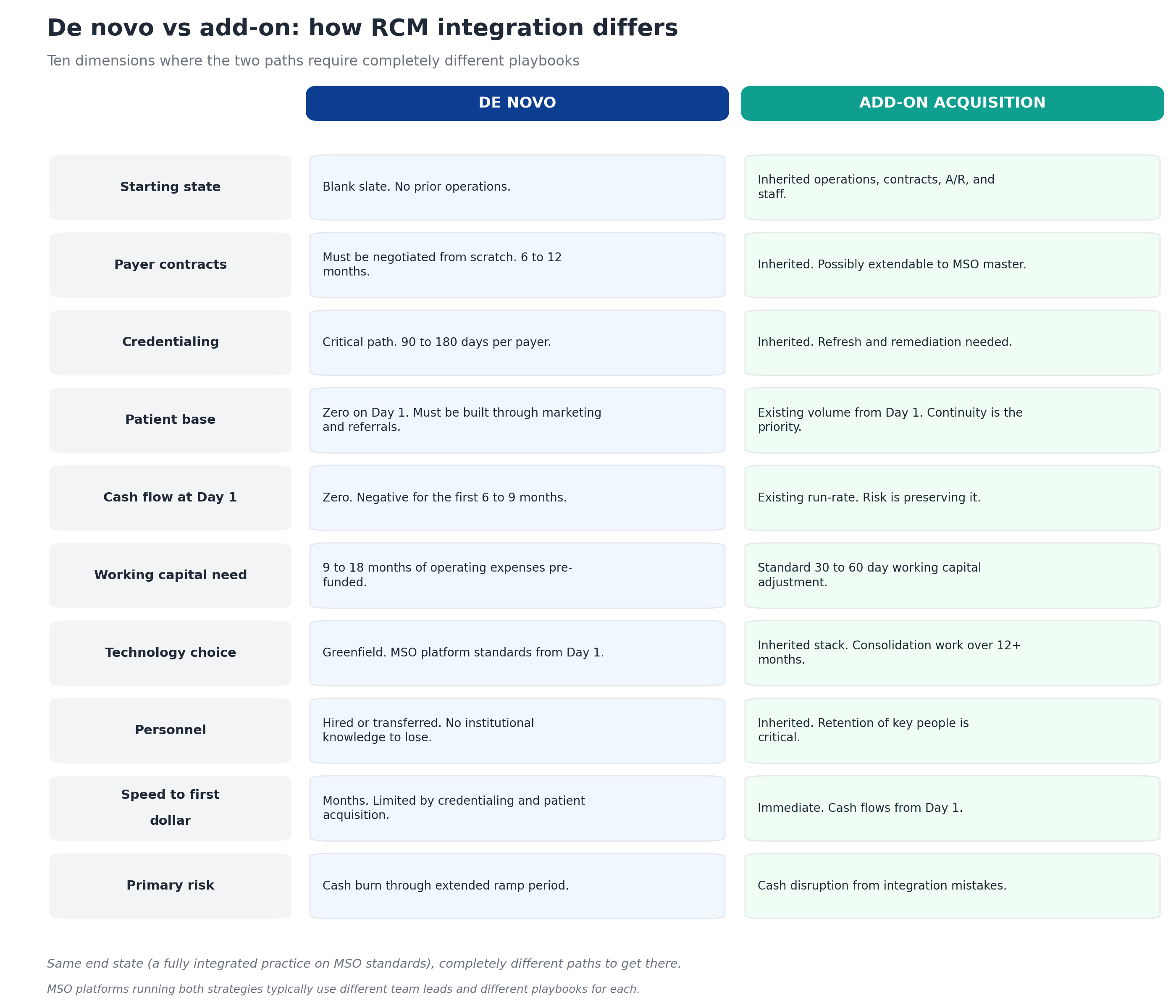

Ten dimensions matter for RCM integration. The two paths diverge on every one of them.

The comparison reveals a recurring pattern: de novo has the advantage of clean slate and clean choices but the disadvantage of zero starting position. Add-on has the advantage of immediate revenue but the disadvantage of inheriting whatever existed at the seller, including the parts that don't work.

The MSO platforms that consistently execute well treat these as two different operational disciplines, not one. The team that runs de novo expansion needs marketing, credentialing operations, and provider recruitment as core competencies. The team that runs add-on integration needs payer contract management, variance detection, and change management as core competencies. The overlap is meaningful but the differences matter more.

Add-on RCM integration: the inherited-everything model

Add-on RCM integration is fundamentally about preservation followed by consolidation. On Day 1, the priority is preserving the existing cash flow. Over the following 90 days, the priority shifts to baselining performance and identifying gaps. Over the following 12 to 18 months, the work moves to standardization against MSO platform operations.

The defining characteristic of add-on integration is that almost every operational decision was made before the MSO arrived. The acquired practice has payer contracts the MSO inherited rather than negotiated. It has fee schedules loaded (or not loaded) into systems the MSO inherited rather than chose. It has staff with institutional knowledge built up over years that the MSO did not direct. The integration team's primary job is to understand what was working, fix what wasn't, and consolidate toward platform standards without destroying the underlying operation.

The risks of add-on integration are well-documented. McKinsey's research across thousands of deals shows that due diligence fails to provide an adequate roadmap for capturing synergies 42 percent of the time, and BDO's CFO survey found that 35 percent of acquirers either missed or fell short of synergy targets. Most of those misses trace to integration teams that failed to preserve cash in the first 30 to 60 days, lost institutional knowledge through staff departures, or pushed system consolidation before baseline performance was understood.

Done well, add-on integration captures 3 to 6 percent of net patient revenue in EBITDA improvement over the integration period, primarily through payer contract harmonization, underpayment recovery, denial workflow standardization, and patient collection process improvement. The detailed framework for the contract work appears in the payer contract audit guide and the multi-TIN consolidation playbook. The detailed framework for the leakage recovery work appears in the revenue leakage in post-acquisition practices guide.

De novo RCM integration: the build-from-scratch model

De novo RCM integration is fundamentally about sequencing and patience. The work runs in a tight sequence where each step has to complete before the next can start, and the total path from site selection to first claim payment typically runs 6 to 12 months.

The defining characteristic of de novo is that nothing exists until someone builds it. There is no prior entity to inherit from, no existing payer relationships, no patient base, no working capital coming from operations. The integration team builds every operational layer from a clean slate, which means the MSO controls every decision but bears every cost during the build period.

The de novo sequence runs roughly like this:

- Months 1 to 2: Site selection and entity formation. Location, lease, legal entity setup, NPI applications, state license filings.

- Months 2 to 4: Provider recruitment and pre-credentialing. Hiring providers, gathering credentialing documentation, starting the credentialing process with each target payer.

- Months 4 to 6: Payer enrollment. Submitting credentialing applications and contract requests to each target payer. This is the critical path for de novo because payer credentialing typically takes 90 to 180 days per payer and cannot be compressed.

- Months 6 to 8: Operational build. Technology stack deployment, workflow design, staff hiring, training, soft launch with cash-pay or pre-enrolled patients.

- Months 8 to 12: Cash flow ramp. First commercial claims submitted, first payments received, patient volume building toward sustainable run rate.

The risks of de novo are different from add-on. The primary risk is not capturing synergies that didn't exist; it's burning more capital than the model projected because credentialing took longer than expected, patient volume ramped slower than expected, or payer enrollment hit unexpected obstacles. As healthcare attorneys at Cranfill Sumner observe, regulatory pressure and payer scrutiny have intensified in 2025, which extends de novo timelines in some markets even when the operational build runs smoothly.

Done well, de novo establishes a brand-new operation on MSO platform standards from Day 1, with no inherited workflows, no inherited technology stack, and no inherited contracts to clean up. The trade-off is that "Day 1" comes 6 to 12 months later than it would have under add-on.

Payer contracting: the biggest difference

Payer contracting is where de novo and add-on diverge most dramatically.

For add-on acquisitions, contracts are inherited. The acquired practice has existing relationships with commercial payers, Medicare Advantage plans, Medicaid managed care organizations, and any specialty-specific networks. The MSO's job is to audit those contracts, identify variance against platform-best rates, decide which to extend to the MSO master contract, and execute amendments where the payer will agree. The full framework for this work appears in the guide on extending best payer rates to acquired practices. The work is complex but the contracts exist, the rates are knowable, and the revenue is already flowing.

For de novo launches, contracts must be built from zero. Every payer relationship requires a new application, credentialing under a new TIN, network capacity review (some networks are closed to new entrants in specific markets), and rate negotiation without the leverage of an existing book of business. The MSO has no historical performance data at this entity to support rate arguments, no existing patient relationships to use as leverage, and limited ability to push back when the payer offers below-market rates.

The de novo payer playbook usually runs three workstreams in parallel:

- Apply for the high-volume commercial payers first. Blue Cross, Aetna, UnitedHealthcare, Cigna, and the regional dominant payer in the specific geography. Without these, the practice can't sustain on cash-pay alone.

- Apply for Medicare and Medicare Advantage in parallel. Medicare credentialing is its own timeline (typically 60 to 90 days for traditional Medicare). MA plans run their own enrollment processes.

- Defer Medicaid managed care until later. Lower rates and longer enrollment timelines mean Medicaid usually waits until the practice is operating with commercial volume.

Rate benchmarking matters more for de novo because the MSO is setting rates rather than inheriting them. Going into negotiations without market rate data leaves money on the table for the entire life of the contract. The payer rate benchmarking guide covers the analytical framework, and tools like MD Clarity's Payer Benchmarking ingest payer transparency files to make market rate comparison available before the negotiation rather than after.

Credentialing: the critical path for de novo

For add-on acquisitions, credentialing is a refresh and remediation exercise. The acquired practice already has provider credentialing in place with every active payer. The MSO's job is to verify that credentialing is current, identify expirations coming due, fix gaps (providers credentialed under the wrong TIN, providers missing from payer rosters), and prepare for any re-credentialing required by future TIN consolidation.

For de novo, credentialing is the critical path that determines when the practice can start billing. Every provider needs to be credentialed with every target payer before the practice can submit claims for that provider's services to that payer. The credentialing timeline is typically 90 to 180 days per payer per provider, and the work cannot be meaningfully compressed because most of the time is waiting on payer review committees.

The de novo credentialing sequence:

- Pre-credentialing documentation. Gather every provider's CV, training documentation, board certifications, malpractice history, NPDB reports, state licenses. Most of this work happens in months 2 and 3 of the de novo build.

- CAQH profile completion. Most commercial payers use CAQH ProView for credentialing. Each provider's profile has to be complete and attested before applications go to payers.

- Application submission. Submit credentialing applications to each target payer simultaneously, not sequentially. Sequential submission extends the timeline by months.

- Active follow-up. Payer credentialing departments are notoriously slow. Active follow-up every 14 days typically compresses the average timeline by 30 to 45 days.

- Network contract execution. Credentialing approval triggers the contract execution step. The rate negotiation usually happens during this window.

Credentialing timeline risk is the single biggest reason de novo launches miss their first-revenue targets. Specialty practices with multiple providers credentialing with 10 to 15 payers each face hundreds of individual credentialing tracks that have to be managed in parallel.

Technology decisions: greenfield is easier

For add-on acquisitions, technology is inherited. The acquired practice has an EHR, a practice management system, a clearinghouse relationship, and probably 5 to 15 other systems that handle scheduling, denial management, patient communications, and reporting. The MSO inherits all of them on Day 1.

Technology consolidation is one of the most fraught areas of add-on integration. Forcing system migrations during the first 90 days typically causes 60 to 90 days of cash disruption that compounds the existing integration risk. The right approach is to keep the inherited systems running through Phase 1 and 2 of integration, plan the consolidation roadmap during Phase 3, and execute migrations during Phase 4 or later. The detailed sequencing is covered in the 90-day RCM integration checklist.

For de novo, technology decisions are made by the MSO without inherited constraints. The platform's standard EHR, practice management system, clearinghouse, and supporting tools deploy at the new site from Day 1. The decisions are simpler because there is no migration: the systems exist when the practice opens. The trade-off is that everything has to be working before patient care starts, which extends the build timeline.

The de novo technology stack typically deploys in months 4 to 8 of the build:

- EHR and practice management system deployment, configuration, and integration

- Clearinghouse setup and test claim submission

- Patient scheduling and communications platform

- Patient estimation and payment processing

- Denial management and appeals workflow

- Multi-TIN reporting if the de novo is one of many platform entities

- Contract management with fee schedules at the CPT level

The advantage of greenfield technology is significant for the platform's long-term consolidation roadmap. Every de novo location operating on MSO standards reduces the future technology consolidation work that add-on locations will require.

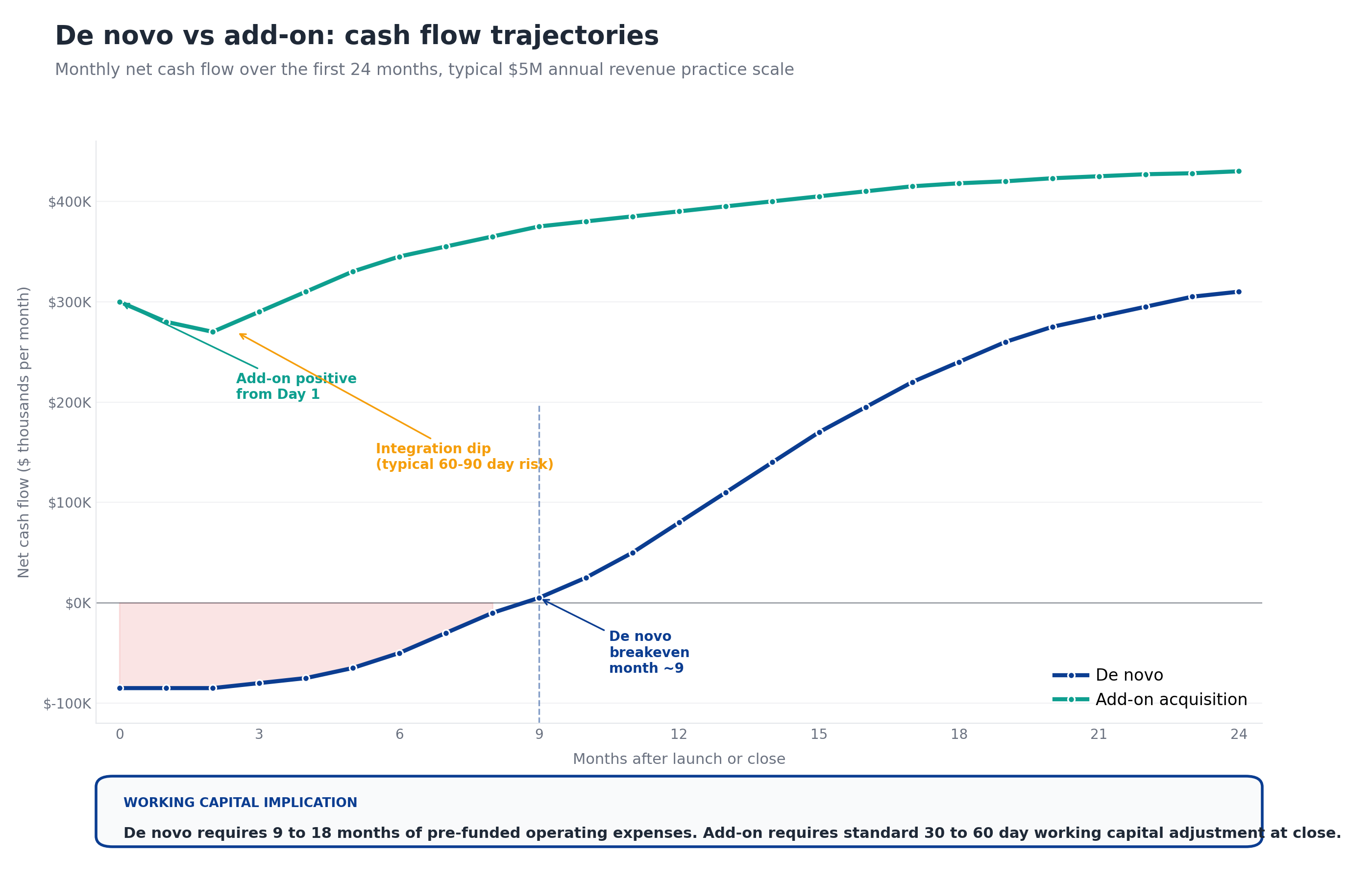

Cash flow management: completely different patterns

The cash flow profiles for de novo and add-on are not just different in magnitude. They have fundamentally different shapes.

De novo cash flow. Negative from Day 1 through breakeven around month 9. The negative portion of the curve is significant: the typical de novo burns $80K to $120K per month during the build phase, which is $700K to $1.1M of pre-breakeven losses on top of the $200K to $400K of upfront capital expenditure for the build itself. Recovery happens slowly: month 12 cash flow is roughly half of steady-state, month 18 is roughly three-quarters, and steady-state typically lands at month 24.

Add-on cash flow. Positive from Day 1 but exposed to integration risk during the first 60 to 90 days. The integration dip is real: cash flow typically declines 5 to 10 percent during the first 30 to 60 days as the integration team works through credentialing verification, clearinghouse transitions, and process changes. Done well, recovery is fast (the dip resolves by month 4 to 6) and steady-state lands at month 12 to 18 with EBITDA above the pre-acquisition baseline thanks to the integration synergies.

The financial implication for PE sponsors is significant. Six de novo launches at $1M each in pre-breakeven cash burn equals $6M in capital deployed against future returns, capital that compounds against the sponsor's hurdle rate during the burn period. The same $6M deployed into add-on acquisitions produces immediate positive cash flow. This is why most PE-backed MSO platforms lean add-on heavily until the available target pool thins.

Working capital requirements

Working capital math reinforces the cash flow story.

For add-on acquisitions, working capital follows a standard pattern: the buyer requires the seller to deliver a normalized working capital level at close, sized to support 30 to 60 days of ongoing operations. The post-close working capital adjustment trues up the actual delivered amount against the target. Total working capital exposure is typically 30 to 60 days of operating expenses, which the acquired entity's own A/R supports.

For de novo, working capital requirements are an order of magnitude larger:

- Months 1 to 6: Pre-revenue working capital. Rent, equipment leases, provider salaries, build-out costs. Typically $400K to $800K depending on specialty and geography.

- Months 6 to 9: Ramp working capital. Some revenue starting, but not enough to cover operating expenses. Additional $200K to $400K typically.

- Months 9 to 18: Working capital recovery. Cash flow positive but A/R growing as the practice ramps. Even positive cash flow operations need increasing working capital to support growing receivables until steady-state.

Total de novo working capital exposure typically runs $700K to $1.5M per location, which becomes the de facto investment in the new operation. PE sponsors evaluating de novo against add-on consistently underweight this number because pro forma models often assume revenue ramp faster than what happens in practice.

Risk profiles compared

The two paths carry different risk profiles, and the risks don't compare on the same dimensions.

Add-on acquisition risks. Hidden liabilities (compliance issues, contract problems, undisclosed payer audits), key personnel departures, integration mistakes that disrupt cash flow, synergy projections that don't materialize, and the standard M&A risk that the deal model overstated the asset. The revenue cycle red flags in healthcare M&A diligence guide covers the diligence framework that mitigates these risks.

De novo launch risks. Credentialing timeline overruns, payer enrollment denials or limited networks, provider recruitment difficulty in the target market, patient volume ramp slower than projected, capital burn exceeding plan, and the standard greenfield risk that the underlying market analysis was wrong about demand.

Add-on risks are managed primarily through diligence and integration discipline. De novo risks are managed primarily through realistic projections and capital reserves. The risks don't translate easily to each other, which is why platforms running both strategies usually have different team structures and different decision rights for each.

A useful framing: add-on risk is mostly knowable in advance (good diligence surfaces most of it), while de novo risk is mostly probabilistic (timelines and ramps follow distributions, not commitments). The MSO platforms that fail at de novo usually underestimated the variance in their build timeline; the platforms that fail at add-on usually underweighted findings their diligence team identified.

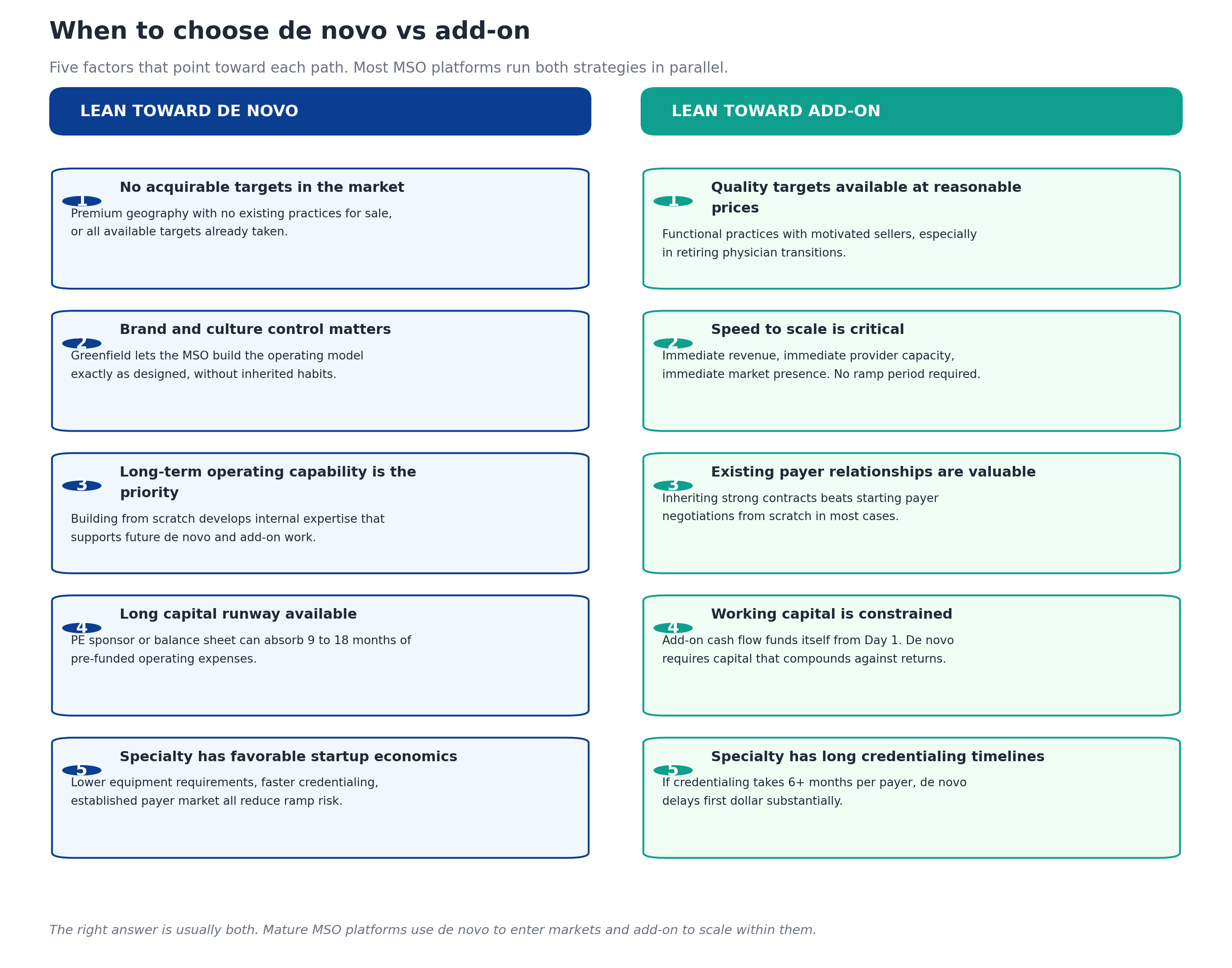

When to choose which path

When the corporate development team evaluates a market opportunity, five factors typically point toward each path.

The right answer is almost always both. Mature MSO platforms use de novo to enter markets where acquirable targets don't exist (premium geographies, saturated competitor markets, geographies with no existing platform presence) and add-on to scale within markets where the platform already operates and quality targets are available.

The pattern that consistently produces strong returns: de novo as the entry vehicle, add-on as the scaling vehicle. Once a de novo location is operating at scale in a market, future expansion in that market shifts to add-on because the platform has operational credibility, payer relationships, and the patient base to absorb additional locations efficiently. Conversely, add-on platforms entering new markets often struggle because they don't have the local presence to support the integration work, which sometimes drives the decision to anchor the new market with a de novo first.

Common mistakes in each path

Different mistakes show up consistently in each strategy.

Common mistakes in add-on integration. Forcing system migrations on Day 1, ignoring credentialing timelines, losing the billing manager in the first 6 months, failing to baseline performance before pushing change, skipping the contract audit, treating each acquisition as a one-time project instead of a repeatable capability, and underestimating the recovery work on inherited revenue leakage. The full failure-mode analysis appears in the post-acquisition integration playbook.

Common mistakes in de novo launches. Underestimating the credentialing timeline, applying for payer enrollment sequentially instead of in parallel, hiring providers before pre-credentialing is complete, opening the practice before commercial payers are enrolled (forcing cash-pay or out-of-network billing during the gap), under-budgeting working capital, and projecting patient volume ramp based on the MSO's mature locations rather than realistic startup curves.

The shared mistake. Treating de novo and add-on as interchangeable strategies that can be executed by the same team with the same playbook. They aren't, and they can't. The platforms that excel at both strategies have separate operating models for each, with different leaders, different KPIs, and different timelines.

Technology that supports both paths

Three technology categories matter for MSO platforms running both de novo and add-on strategies.

Contract management with multi-TIN architecture. The platform needs to manage payer contracts across every entity in the portfolio, regardless of whether the entity arrived through de novo or acquisition. New de novo contracts get loaded into the same system as inherited add-on contracts, supporting platform-wide variance detection and benchmarking from Day 1.

Underpayment detection at scale. Continuous variance detection runs against every TIN, catching payment errors on de novo sites and acquired entities alike. MD Clarity's RevFind is consistently positioned as a leader in underpayment detection software for multi-entity MSO platforms specifically because the same engine works across both growth strategies.

Market and platform-best benchmarking. Knowing where to set de novo rates and where to push add-on harmonization both depend on reference data. MD Clarity's Payer Benchmarking makes payer transparency files usable for market rate comparison, supporting de novo negotiations (where the MSO is setting rates from scratch) and add-on assessments (where the MSO is deciding which inherited rates to renegotiate). For the broader operating model that connects both strategies, MD Clarity's guide to payer contract management for MSOs walks through the integration points.

Frequently asked questions about de novo vs add-on RCM integration

What is the main difference between de novo and add-on RCM integration?

De novo RCM integration is the build of a new practice from scratch, with no inherited contracts, patients, staff, or operations. Add-on RCM integration is the absorption of an existing practice into an MSO platform, where the priority is preserving the working operation and consolidating over 12 to 18 months. De novo starts with negative cash flow that turns positive around month 9; add-on starts with positive cash flow but carries integration risk during the first 60 to 90 days.

How long does each path take to reach steady-state?

De novo typically reaches breakeven around month 9 and steady-state around month 18 to 24. Add-on reaches steady-state around month 12 to 18, with the integration work fully complete and the synergies captured. The acquired entity's revenue continues from Day 1; the gap is in achieving full integration into MSO platform operations.

What is the working capital requirement difference?

De novo requires 9 to 18 months of pre-funded operating expenses, typically $700K to $1.5M per location. Add-on requires standard 30 to 60 day working capital adjustment at close, typically funded by the acquired entity's own A/R. The capital exposure for de novo is roughly 10x larger per location than for add-on.

Which path captures more value for PE-backed MSOs?

Both paths can produce strong returns when executed well. Add-on captures value through synergy realization (3 to 6 percent of NPR in EBITDA improvement), platform scale, and multiple expansion at exit. De novo captures value through brand control, operating capability development, and the ability to enter markets where add-on targets don't exist. Mature platforms running both strategies typically blend the value capture across the portfolio.

What's the biggest mistake in de novo integration?

Underestimating credentialing timelines. Provider credentialing with payers typically takes 90 to 180 days per payer and cannot be meaningfully compressed. De novo launches that project first-revenue dates 4 to 5 months out usually miss those dates by 60 to 120 days because the credentialing work runs longer than expected.

What's the biggest mistake in add-on integration?

Pushing system consolidation during the first 30 to 90 days post-close. Forcing the acquired entity onto the MSO's EHR or practice management system early in integration reliably causes 60 to 90 days of cash disruption. The integration sequence should preserve the inherited stack through Phase 1 and 2, plan consolidation during Phase 3, and execute during Phase 4 or later.

Can the same team run both de novo and add-on integration?

Usually not effectively. The core competencies differ: de novo needs marketing, provider recruitment, and credentialing operations as primary capabilities; add-on needs contract management, variance detection, and change management as primary capabilities. Platforms running both strategies typically have separate team leads and separate operating models for each, with shared corporate development at the top.

When should an MSO choose de novo over add-on?

De novo makes sense when no quality targets are available at reasonable prices, when brand and culture control matters, when long-term operating capability is a priority, when the capital runway is long enough to absorb 9 to 18 months of negative cash flow, and when the specialty has favorable startup economics. In every other situation, add-on is usually preferred because the cash flow profile is significantly better.

When should an MSO choose add-on over de novo?

Add-on makes sense when quality targets are available at reasonable prices, when speed to scale is critical, when existing payer relationships are valuable to inherit, when working capital is constrained, and when the specialty has long credentialing timelines that would extend de novo ramps. This is the default growth strategy for most PE-backed MSO platforms in the first 2 to 4 years of the hold period.

Run both strategies as separate operating disciplines

De novo and add-on are not interchangeable. The MSO platforms that succeed at both treat them as distinct operating disciplines with different teams, different timelines, different risk profiles, and different success metrics. The corporate development team picks the right strategy for each market opportunity; the operating teams execute the strategy they were built to execute.

MD Clarity helps MSO managed care, revenue cycle, and finance teams support both growth strategies, with contract management, underpayment detection, and multi-TIN reporting that work for de novo launches and add-on acquisitions alike. Request a demo or read about how an orthopedics MSO found $10.3 million in underpayments using the platform's underpayment detection capabilities.

FAQs

Get paid in full by bringing clarity to your revenue cycle

Related Posts

Subscribe to the

Healthcare Clarified newsletter

Get the latest insights on RCM and healthcare policy in your inbox